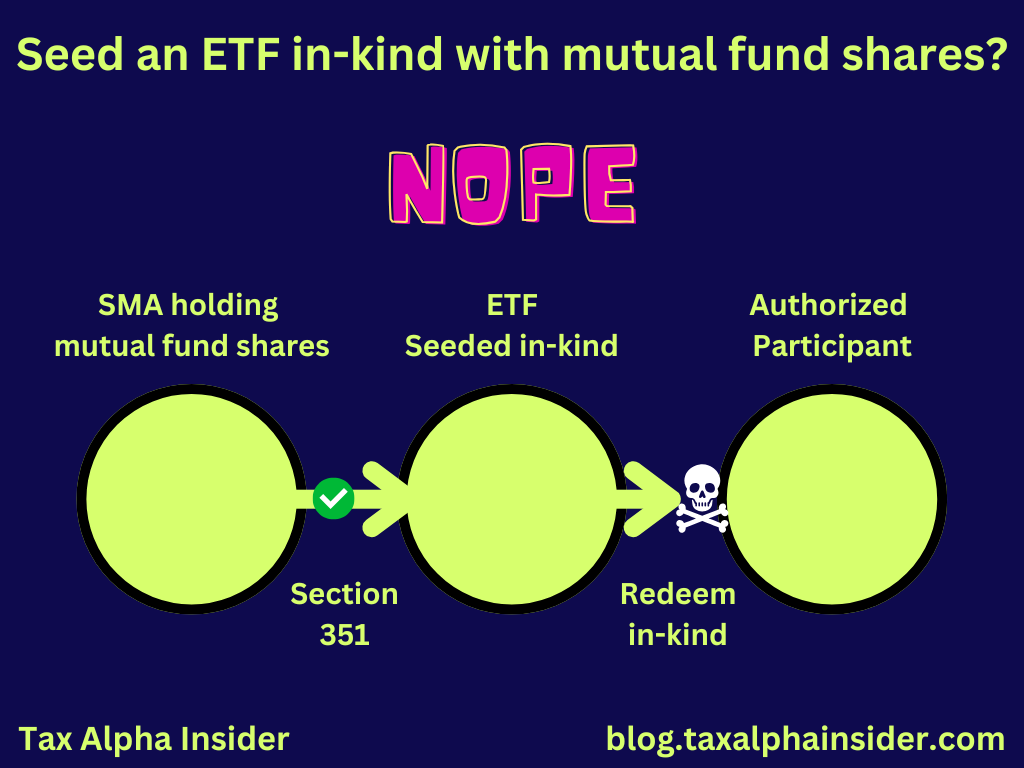

Can I seed an ETF in-kind using mutual fund shares?

Technically, yes, but no ETF will take it.

I’ve written a lot about the Section 351 transfer to an ETF.

Here is my explainer. And here is a live webinar I hosted with Meb Faber, whose Cambria Tax Aware ETF (TAX), seeded in-kind, goes live next week.

Section 351 allows investors to transfer diversified assets (this is not a single stock de-risking solution) into the ETF wrapper without immediate tax consequences.

By far, the most common question folks have asked me is, “Can I use Section 351 to transfer mutual fund shares into the ETF wrapper?”

Technically, yes, but practically, no.

Mutual funds shares are cash-in-cash-out, meaning authorized participants (APs) cannot redeem them in-kind.

While there are no legal or technical barriers to transferring mutual fund shares in-kind since they can’t be redeemed in-kind, rebalancing and redeeming will trigger capital gains tax, requiring distribution.

The ETF sponsor does not want that and will almost always reject mutual fund share contributions.

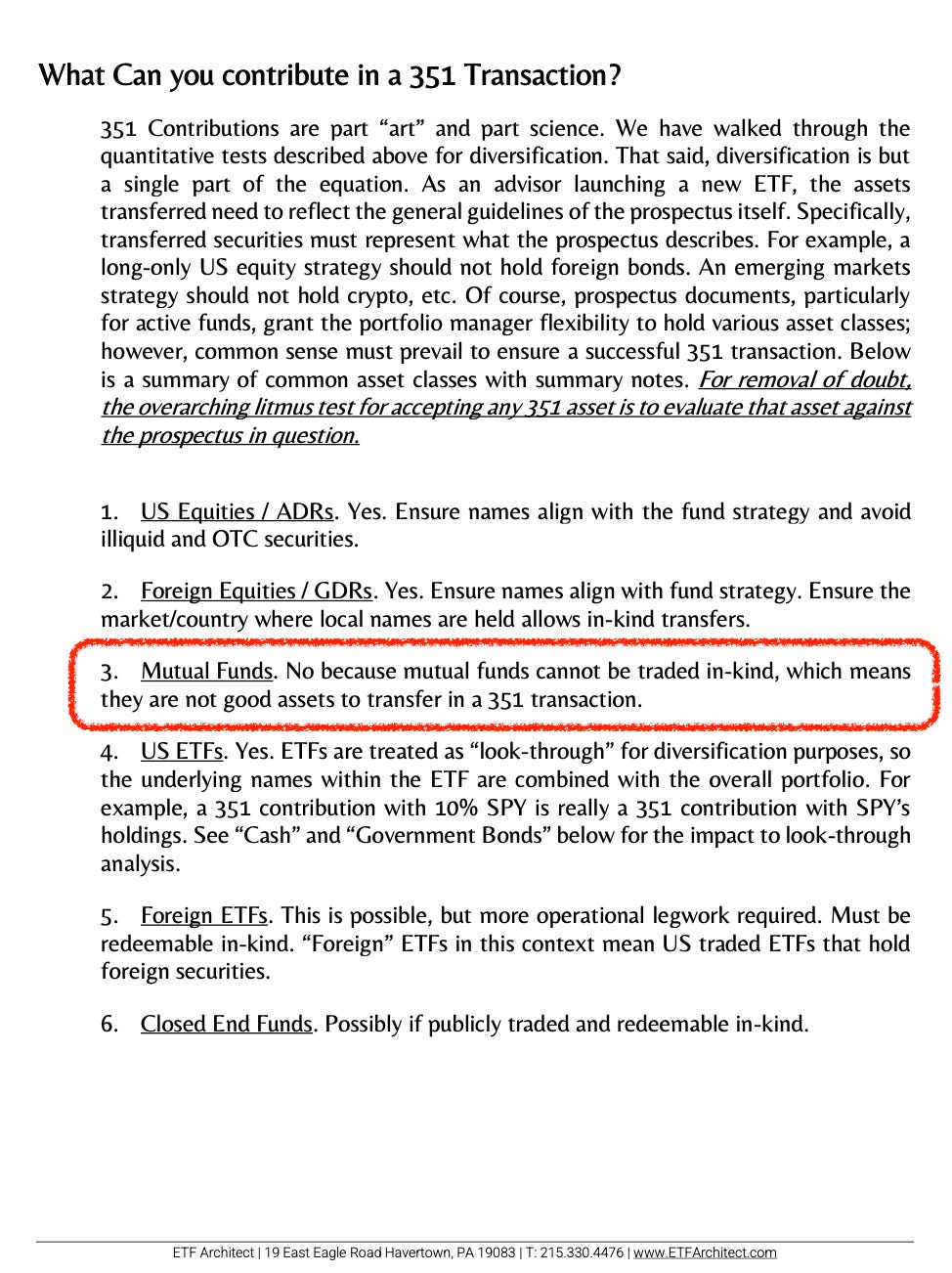

In any case, here’s ETF Architect saying the same thing.

Here’s ETF Architect’s Intro to ETF Taxation and 351 Conversions for future reference.

In case you’re wondering… mutual funds converting to ETF (also via section 351) and mutual funds introducing ETF share classes (a' la Vanguard) will help solve the mutual fund lock-up problem.