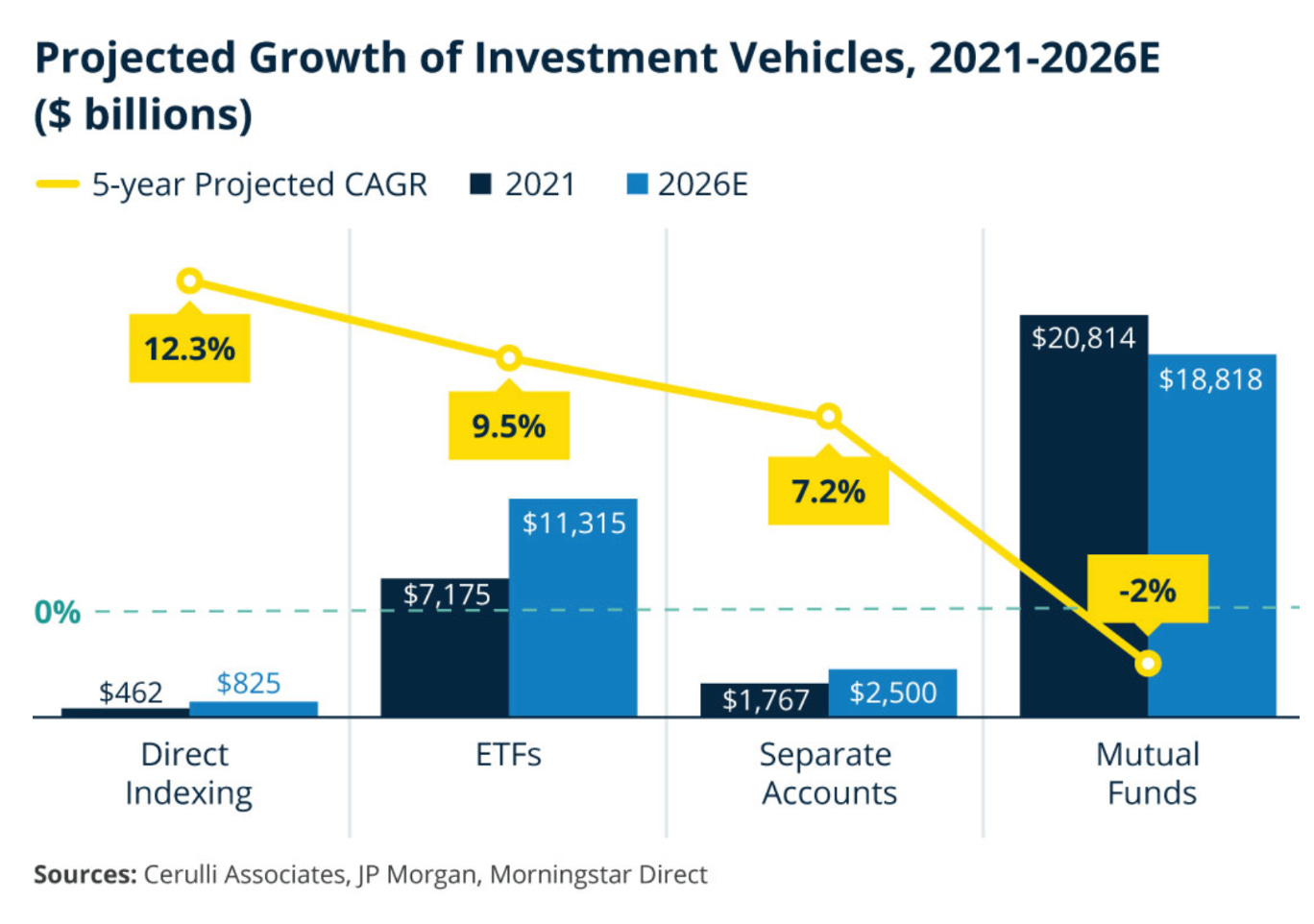

Direct Indexing Is Not A Rocket Ship

ETFs are a formidable alternative

Tax Alpha Weekly

Partners Capital: The After-Tax Investment Lens

Brooklyn: Scaling Separate Account Management with Generative AI

Smartleaf: Yes, Direct Indexes Make Sense for Investors Worth Less Than $1mm and Over $5m (a response to my LinkedIn post)

Morningstar (credible rumor): Shutting down its direct indexing product

Leader: Direct Indexing Is Not A Rocket Ship

In Dec 2022, Cerulli predicted direct indexing would grow faster than ETFs. I’m not buying it.

Direct indexing is effective, but ETFs are simple

My crazy idea was just to ask questions.

Rather than arguing with advisers about the tradeoffs of direct indexing versus ETFs, I would just listen to what they (not vendors) had to say. I was surprised.

For instance, many advisers shrugged off direct indexing. “The juice isn’t worth the squeeze” and “It’s a gimmick” were common refrains.

Few doubted that direct indexing produced incremental tax alpha or that portfolio customization could be helpful for risk mitigation and personalization.

But this stuff didn’t move the needle for the holdouts.

Many were very concerned about sampling the portfolio, “Where’s the NVDA?” and experiencing/explaining tracking error, while others didn’t want to work with yet another vendor and couldn’t see the point for small (or low tax bracket) clients.

To be fair, the strongest holdouts were relatively small practices that claimed to be growing just fine without direct indexing.

However, a few growth-oriented advisers, north of $1 BN AUM, told me they didn’t think direct indexing would win them any new business.

Cannibals

Another, albeit smaller, headwind is that tax-aware long/short SMAs and hedge funds cannibalize business from the plain-vanilla direct indexing world.

Think about it: An adviser has already bought into the idea of tax alpha, separate accounts, tracking error, etc. In other words, they are the ideal prospect for a direct indexing vendor. But then they learn about tax-aware long/short and get curious. Many will pass, but a few will choose it over direct indexing.

Fidelity and Interactive Brokers are mostly the only custodians paying a short rebate sufficient to support 130/30 and similar strategies, but someone told me Charles Schwab might start too. If true, advisers with less than $100 million AUM could soon have access to more sophisticated stuff.

A Formidable Alternative

The bigger picture seems that advisers could afford to shrug off direct indexing because ETFs mostly do the job.

ETFs, after all, remain wildly tax-efficient.

If adviser indifference is a significant headwind for direct indexing, ETFs, by contrast, have some tailwinds:

First, several mutual funds are introducing an ETF share class. My instinct is that transitioning from mutual fund to ETF, sometimes without any effort, will propel ETF growth for a while. It’s much more of a cognitive, marketing, and operations leap from fund to direct index, no matter how simple vendors make it.

It’s also easier for sponsors to experiment with new ETFs. They can throw things at the wall and see what sticks.

What now?

To be clear, plenty of business exists for direct indexing vendors. This piece makes zero arguments about the merits of direct indexing over ETFs. This is about market structure, differentiation, and friction (or lack thereof).

My point is that finding advisers who lean into direct indexing rather than shrugging might be a little tougher than originally predicted. But they are out there, and knowing why they shrug should help inform a vendor’s sales and marketing motion.

Finally, direct indexing is much earlier in its adoption lifecycle than the ETF wrapper, which has achieved mainstream status. And many large asset managers entering the SMA game haven’t figured out how to sell it yet (you know who you are). This should give direct indexing room to accelerate, the argument goes.

But ETFs will grow too. And I think they have the upper hand for now.