De-risking concentrated stock by seeding an ETF in-kind

Up to 25% could come from a single stock.

“Can I seed a new ETF in-kind with one stock?”

The answer is no. And the reason is (lack of) diversification.

However, once the diversification tests are passed, a hypothetical investor could contribute up to 25% of a remaining concentrated position to a new ETF without incurring tax.

This makes Section 351 conversion another important tool in the playbook for managing concentrated positions.

Diversification

Whether or not seeding an ETF in-kind works hinges on diversification.

“Diversified” is defined in the IRC, and much has been written about it.

Assuming each investor and the new ETF are diversified before the transfer, nobody pays tax on the conversion. This is what Meb Faber’s Cambria Tax Aware ETF (TAX) launched last week sought to achieve.

Under ideal circumstances, an individual investor could convert a diversified portfolio, including up to 25% of a single stock, without recognizing capital gain.

How does this work?

De-risking is not diversification

Section 351 of the IRC allows tax-free share transfers to a corporation without triggering capital gains tax.

You can read the basic rules for pulling off a Section 351 conversion to a RIC here.

The most relevant provision for de-risking a concentrated position is that the assets investors transfer must already be diversified.

Testing for diversification is a gauntlet each transferor and fund must pass to prove they are not covertly achieving diversification12 because if “the transfer results in diversification of the transferors’ interests…” then that kills the reason for the in-kind conversion.

Investors cannot “plan” on diversifying using Section 351 in some multi-step scheme3 or purchase Government securities4 to squeeze more of the stock into the ETF seed.

The fund is subject to the 25/50 diversification tests (see example below).

The fund is also subject to the RIC diversification rules after launch.

The point is that if an investor’s contribution is already diversified, there’s no harm in further de-risking while unlocking the cost efficiency, investment selection, and liquidity of the ETF wrapper.

An example of de-risking META shares tax-free

Suppose a large group of investors are each diversified and form a portfolio that looks like this:

$1 million in META stock (25% of the total portfolio)

$3 million in diversified unrelated stocks (75% of the total portfolio, each position ~1%)

25% Rule:

The portfolio passes this rule because META stock accounts for exactly 25% of the total portfolio value, meeting the maximum limit for a single issuer.

50% Rule:

The top five issuers must not exceed 50% of the portfolio’s value.

They sum to ~30% (25% + 5 x 1%) <= 50%.

The portfolio passes the diversification tests.

Assuming all the other provisions are satisfied, the shares transfer in-kind without immediate tax consequences.

Family offices: is diversification relevant?

Suppose a family wants to seed an ETF with $50 million (roughly the ETF operational breakeven) using only a single appreciated stock, and they are the only transferor.

Is the transfer taxable?

In this case, individual investors (the family) “generally” cannot cause diversification.

“If there is only one transferor (or two or more transferors of identical assets) to a newly organized corporation, the transfer will generally be treated as not resulting in diversification.”

That only satisfies the transferor-level diversification test (i.e. no diversification occurred).

However, transferring to a RIC requires fund-level diversification, namely passing the Section 368 25/50 tests5, which a single-stock contribution obviously fails.

And transferring to a RIC requires yet another round of diversification tests to ensure passthrough taxation.

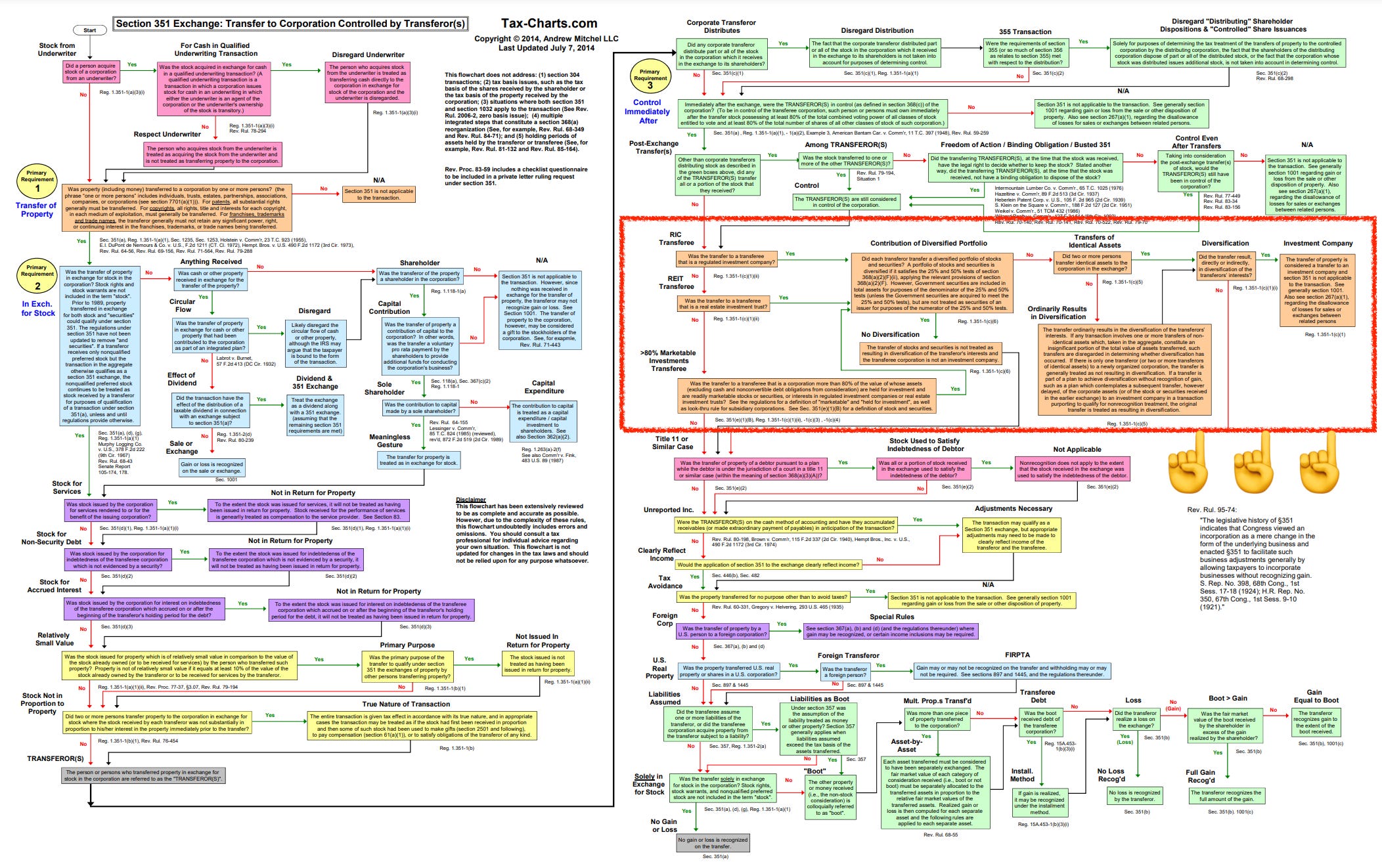

If all of this is confusing, this 351 flow chart is very helpful. The discussion above is on the right side of the image below (in orange, indicated by ☝️☝️☝️… pinch and zoom or just blur your vision and move on).

I included a brief comparison of the three levels of diversification tests in footnotes for nerds6.

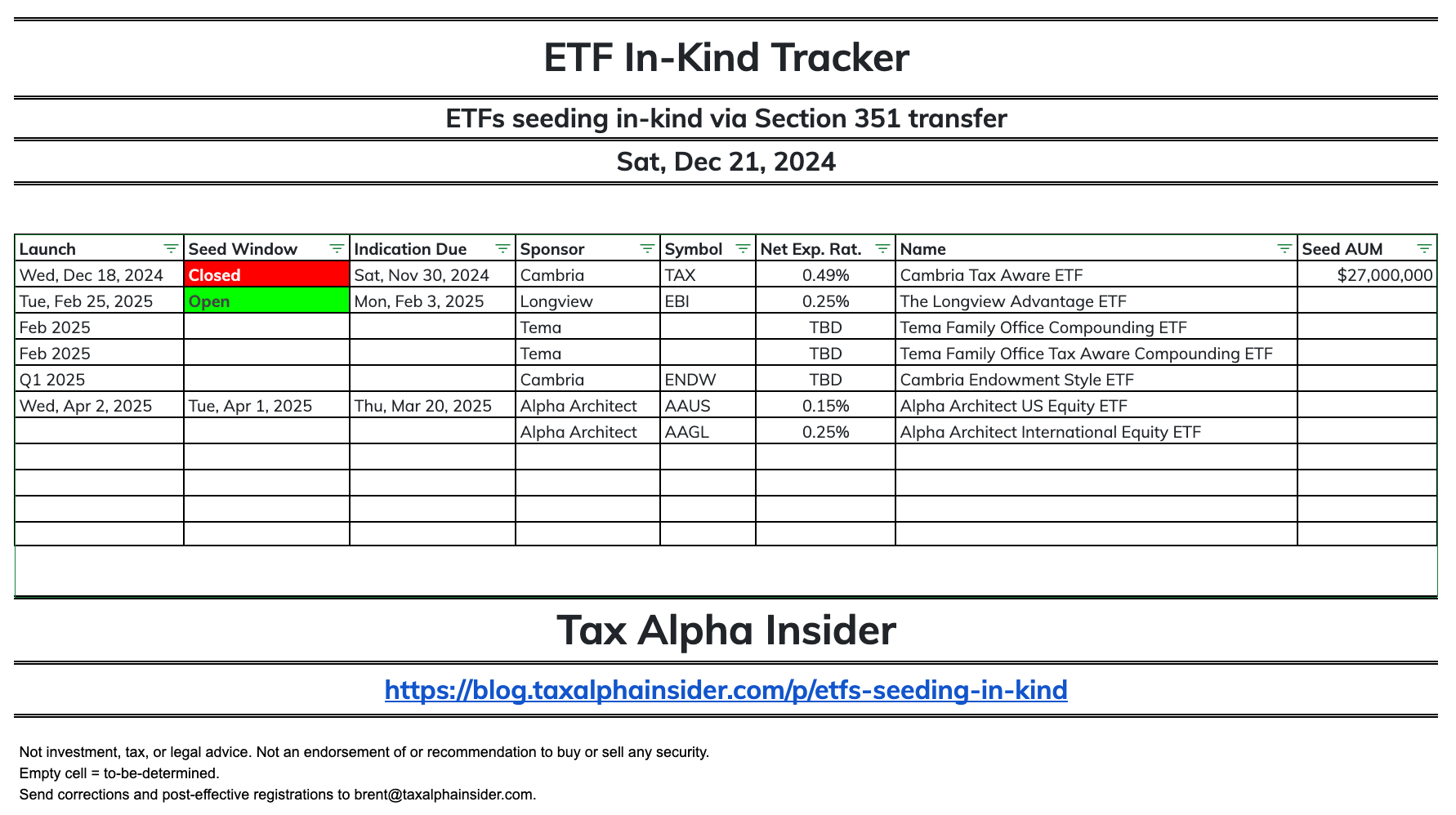

De-risking using Section 351 conversion requires a pipeline of ETFs with seed windows. I’ve been tracking upcoming ETFs seeding in-kind in the following table.

The in-kind ETF pipeline

De-risking depends on ETFs offering in-kind seeding.

Here’s my tracker (bookmark it).

If you know of any ETFs seeding in-kind, tell me about them.

The Cambria Tax Aware ETF seeded last Wednesday with $27 million in-kind.

Here’s my post summarizing the launch.

👋🎄 Tax Alpha Insider is taking a break for a week or two. See you in 2025. 🥳🎉

Disclaimer: This is not investment, tax, or legal advice. Nor is it an endorsement of any investment product or a recommendation to buy or sell any security. This content is educational. Hire a licensed adviser for personalized guidance and to catch any recent changes to the IRC.

The origin of the Exchange Fund… (New York State Bar Association Tax Section Report No. 1252, 2011): Section 351(e) was enacted in 1966 to prevent investors from transferring appreciated marketable stocks and securities to newly formed investment companies, referred to as “exchange funds” or “swap funds”, on a tax-free basis." It continues in a footnote: “…Before this general rule was amended in 1966, the large unrealized gains built into the securities transferred to corporate exchange funds were claimed to be nontaxable to the investors by reason of section 351, since property (the appreciated securities) was transferred to a corporation (the fund) by one or more persons (the investors) solely in exchange for the corporation’s stock or securities (shares of the fund), and such person or persons controlled the corporation immediately after the exchange.”)”

Section 351 conversions require diversification at the transferor level for a fund that will be diversified: “…a transfer of stocks and securities will not be treated as resulting in a diversification of the transferors’ interests if each transferor transfers a diversified portfolio of stocks and securities. 26 CFR Ch. I (4–1–14 Edition)

26 CFR § 1.351-1: “If a transfer is part of a plan to achieve diversification without recognition of gain, such as a plan which contemplates a subsequent transfer, however delayed, of the corporate assets (or of the stock or securities received in the earlier exchange) to an investment company in a transaction purporting to qualify for nonrecognition treatment, the original transfer will be treated as resulting in diversification.”

26 CFR § 1.351-1: “…Government securities are included in total assets for purposes of the denominator of the 25 and 50-percent tests (unless the Government securities are acquired to meet the 25 and 50-percent tests)”

Section 351(e) refers to the diversification rules in Section 368(a)(2)(F)(ii) according to Treas. Reg. § 1.351-1(c)(6): “(6)(i) For purposes of paragraph (c)(5) of this section, a transfer of stocks and securities will not be treated as resulting in a diversification of the transferors’ interests if each transferor transfers a diversified portfolio of stocks and securities. For purposes of this paragraph (c)(6), a portfolio of stocks and securities is diversified if it satisfies the 25 and 50-percent tests of section 368(a)(2)(F)(ii)”

Yes, there are three levels of diversification tests, and here’s a summary:

1. Individual Level (Transferor - Section 351(e))

Purpose: Ensures each transferor contributes a diversified portfolio to avoid taxable diversification.

Test: 25/50 Test from Section 368(a)(2)(F):

No single issuer exceeds 25% of the portfolio.

Top five issuers collectively don’t exceed 50% of the portfolio.

Implication: If the individual fails, their transfer is taxable under Section 351(e).

2. Fund Level (Transferee - Section 351(e))

Purpose: Ensures the receiving fund (corporation/ETF) itself is not an “investment company.”

Test: Same 25/50 Test from Section 368(a)(2)(F).

Applies to the fund’s post-transfer portfolio.

Special Treatment: Government securities are included in the denominator but not the numerator, helping meet the test.

Implication: If the fund fails, the could be taxable for some or all contributors, depending on the circumstances.

3. RIC Level (Ongoing - Section 851(b)(3))

Purpose: Ensures the fund qualifies as a Regulated Investment Company (RIC) for pass-through tax treatment.

Test:

50% Test:

At least 50% of assets in cash, U.S. government securities, other RICs, or securities with:

≤5% of total assets per issuer, and

≤10% of issuer’s voting securities.

25% Test:

No more than 25% of assets in any one issuer or related group.

Implication: Failing this test doesn’t trigger gain recognition but disqualifies the fund as a RIC, losing tax pass-through benefits.