What Is Tax-Aware Long-Short For?

Capital losses. Lots of them.

Tax Alpha Weekly

AQR: Combining VPFs and Tax-Aware Strategies to Diversify Low-Basis Stock [Currently #3 on SSRN’s Top Downloads For Tax Law & Policy]

The Tax Alpha Insider: Is Direct Indexing Active Management?

Leader: What Is Tax-Aware Long-Short For?

When I write about “tax-aware long-short” strategies like the 130/30 or 250/150, readers often write to me about other strategies that are somehow “tax-aware” and “long-short” but not exactly “tax-aware long-short,” as I mean it.

To be “tax-aware long-short,” the strategy must satisfy three criteria:

The implementation wrapper must pass through capital losses to the investor. This eliminates mutual funds and ETFs.

Market exposure must be symmetric. This removes options strategies that introduce convexity.

The leveraged long and short are made up of individual stocks.

If we view investment strategies as tools that solve specific problems, we might say that “tax-aware long-short” seeks tax deferral as a primary objective, not an afterthought (though it might not be marketed as such).

While “tax-aware long-short” strategies may be delivered as extensions or overlays around a concentrated holding or locked-up portfolio, the general case is just direct indexing with less constraints.

The Long-Only Constraint

Direct indexing is a portfolio management strategy. Its beta is symmetric, and it generally mirrors some index or model. Passive or active does not matter these days, and there are no derivatives and no convexity. The strategy is long-only.

Direct indexing tax efficiency comes from two things:

Individual-name holdings

Passthrough taxation of capital losses

Holding individual stocks is a crucial advantage of direct indexing. It enables precision tax-loss harvesting, rebalancing, and gifting.

But there’s no free lunch.

Investors introduce tracking error and omission (or, “Why doesn’t my portfolio hold NVDA?”) risk that some find unacceptable. In many cases, an ETF is the right solution.

Removing The Long-Only Constraint

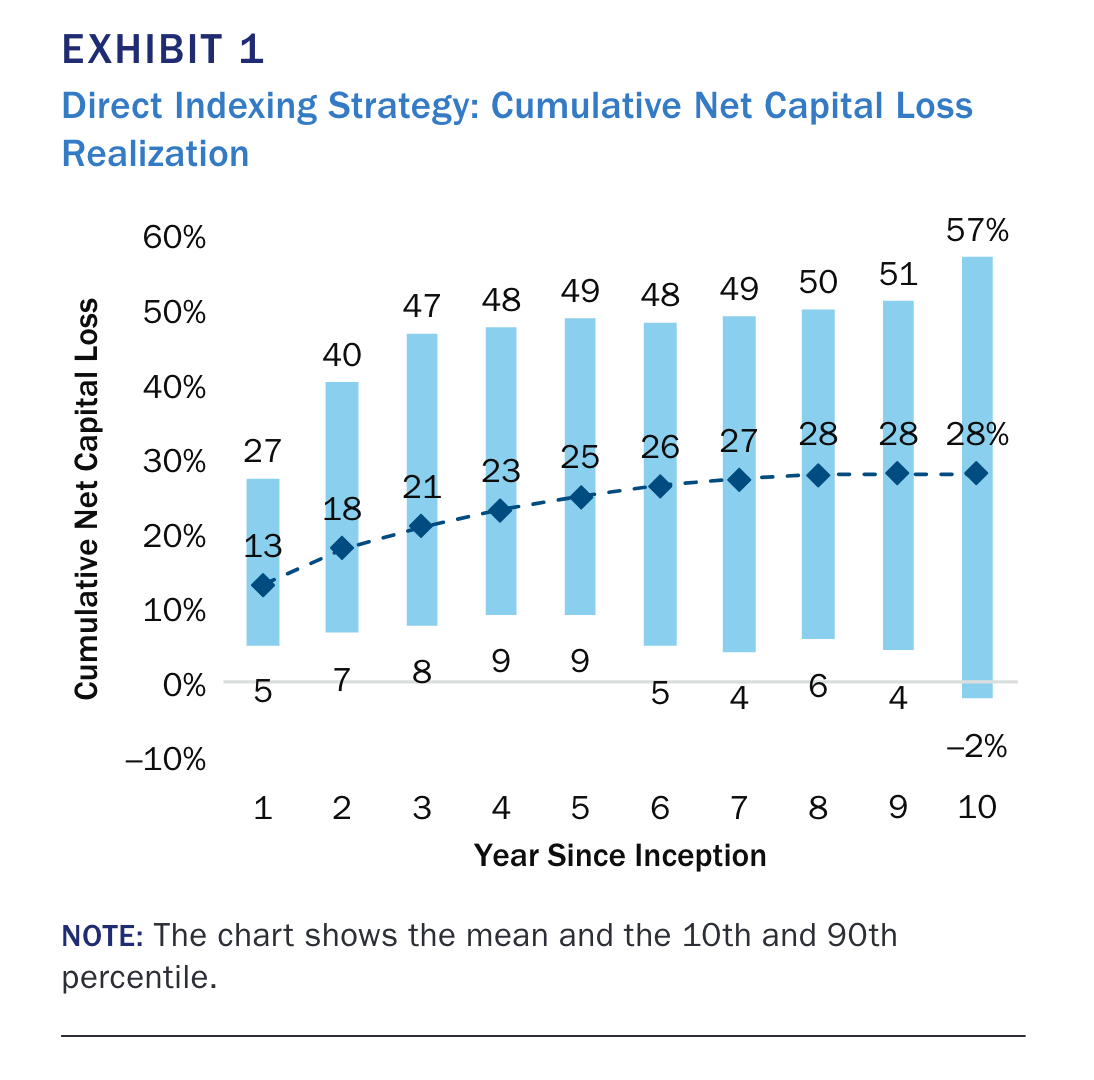

Direct indexing with tax-loss harvesting arrives with a bang. If the markets are volatile and generally down, the portfolio will realize most of its losses around inception. If the market is up, tax-loss harvesting opportunities fall.

After several years, without further cash infusion or extreme volatility, the direct indexing portfolio likely extinguishes its ability to tax-loss harvest. The portfolio is “locked up” and difficult to liquidate or rebalance without realizing significant capital gains.

Suppose an investor uses a direct indexing portfolio to generate capital losses to unwind a concentrated position, as this Vanguard article suggests. In that case, they may be disappointed to read AQR’s research showing that direct indexing may only generate $0.30 or so for every dollar invested over a 10-year simulated stretch.

Liberman, Joseph, Stanley Krasner, Nathan Sosner, and Pedro Freitas. 2023. “Beyond Direct Indexing: Dynamic Direct Long-Short Investing.” https://www.aqr.com/Insights/Research/Journal-Article/Beyond-Direct-Indexing-Dynamic-Direct-Long-Short-Investing.

A concentrated position remains concentrated after ten years.

Extending the long-only mandate solves some of these problems.

Leverage and Shorting

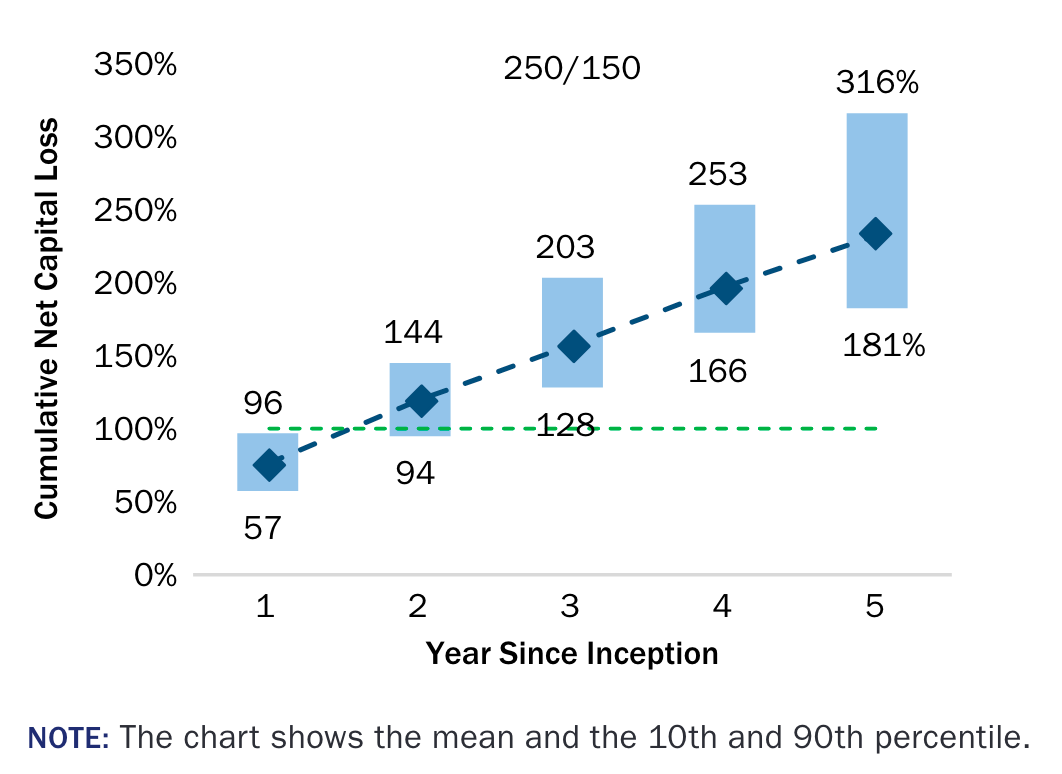

Adding leverage and shorting to a direct indexing mandate increases the “surface area” of the portfolio, and tax-loss harvesting opportunities arrive more consistently in up and down markets.

Many tax-aware long-short implementations offer pre-tax alpha strategies whose trading practices and capital gains realization could be partly funded by the copious capital losses leverage and shorting produce.

AQR has shown simulated losses of around $2.5 for every dollar invested in the five years following inception in a 250/150 implementation.

Liberman, Joseph, Stanley Krasner, Nathan Sosner, and Pedro Freitas. 2023. “Beyond Direct Indexing: Dynamic Direct Long-Short Investing.” https://www.aqr.com/Insights/Research/Journal-Article/Beyond-Direct-Indexing-Dynamic-Direct-Long-Short-Investing. NOTE: This chart shows five years versus ten years shown in the previous chart.

If the investor’s goal is to diversify single-stock concentration tax-efficiently, a long-short mandate outperforms direct indexing by most metrics.

Still Locked Up?

Portfolio lock-up remains unsolved even with leverage and shorting.

When a portfolio, long-only or extended with leverage and shorting, harvests capital losses, the cost basis moves in the opposite direction of the bet.

In other words, harvesting losses in long positions pushes the cost basis down, while harvesting losses in short positions pushes the cost basis up. As we harvest more and more, additional harvesting is less likely.

Investors need to “de-risk” the portfolio eventually.

“To fully unwind a long/short extension that has been successfully used for loss harvesting, some gains need to be realized.” Erkko Etula, the CEO of Brooklyn Investment Group, which manages a tax-aware 130/30 strategy as part of its holistic portfolio solution, tells me.

Since long-short portfolios produce tax losses regularly, “there is typically some room to dynamically adjust leverage over time,” Etula says.

While the AQR paper mentioned a few times above models the planning and transitioning tasks for de-risking a long-short implementation, these are burdens that advisers and portfolios must absorb.

The Right Tool For The Job?

Tax-aware long-short strategies produce capital losses. Though they might offer some pre-tax alpha, investors with significant capital gains now or expecting them in the future, usually select a long-short implementation with tax deferral in mind. However imperfect, if that is the job, tax-aware long-short might be the right tool.

Thanks very informative!