What's in the BOXX? Part 1: State Rates

BOXX (Alpha Architect's 1-3M box spread ETF) gets punished by state income tax. Does it matter?

The Alpha Architect 1-3 Month Box ETF (BOXX) is complicated.

It’s worth a close look because it delivers three significant tax wins in the ETF wrapper:

It accrues capital gains (instead of ordinary income)

It avoids distributing (to reduce tax drag vs. similar ETFs)

When sold, it could be taxed at lower long-term capital gains rates

However, when sold, investors owe tax on all of the accrued value to federal and state authorities.

For comparison, BIL (the SPDR® Blmbg 1-3 Mth T-Bill ETF) receives ordinary income from a portfolio of T-bills and must forward that income to its shareholders. This income is exempt from state income taxes.

We must consider BOXX’s federal tax efficiency vs. its state tax inefficiency.

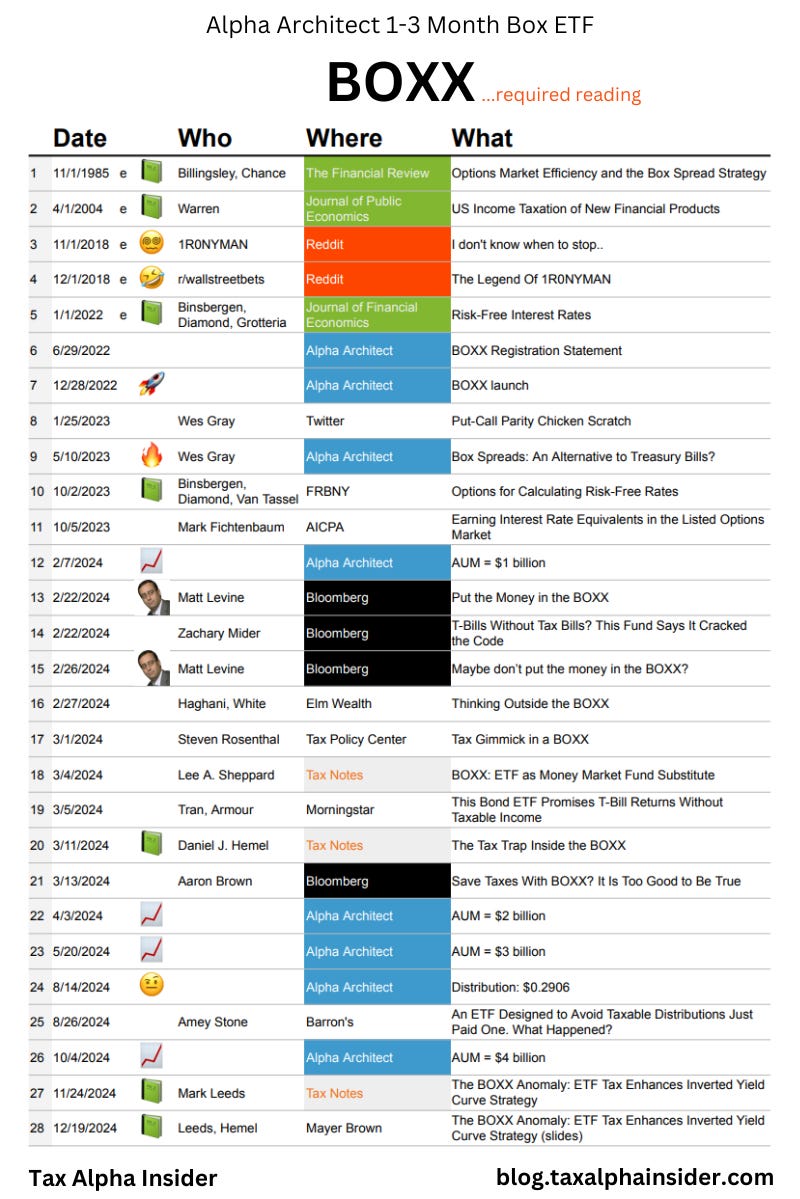

Doesn’t BOXX have bigger fish to fry?

Two lawyers will give a presentation about BOXX in 10 days. They’re debating opposing views on whether obscure provisions in the tax straddle slice of the Code apply and if BOXX is guilty of converting ordinary income into capital gains.

I read the presentation slides and a related Tax Notes article, but BOXX has changed materially in the past 6 months. It’s unclear whether the debate is still relevant. I’m tracking this event and want more info.

Meanwhile, others have written about the incremental credit risk BOXX takes to achieve its four-legged box spread. Or about “LTCM-style meltdowns” and if BOXX would survive.

One critic argues BOXX has no place in a portfolio since it's a T-bill ETF, but it requires holding for more than 1 year to qualify for long-term capital gains rates, and who holds T-bills for more than 1 year? Are bills ever appropriate for long-term investors?

Skyler Weinand, CFA, with Regan Capital told me “With cash yielding over 4.5% and the belly of the curve yielding only 4.1%, investors are right to ‘sit on the sidelines’ and wait for the yield curve to normalize. If anything, they're the smart money in the market (just ask Warren Buffett).”

If you’re curious for background reading on BOXX. Here’s a guide. If you want the spreadsheet just send me a message.

Until now, no one has looked at the state income tax BOXX shareholders must pay that similar ETFs (or primary market purchasers) do not. State income taxes could be a deal breaker, and if so, I want to know about that before doing more work on some of the gnarlier topics I listed above.

State Rates

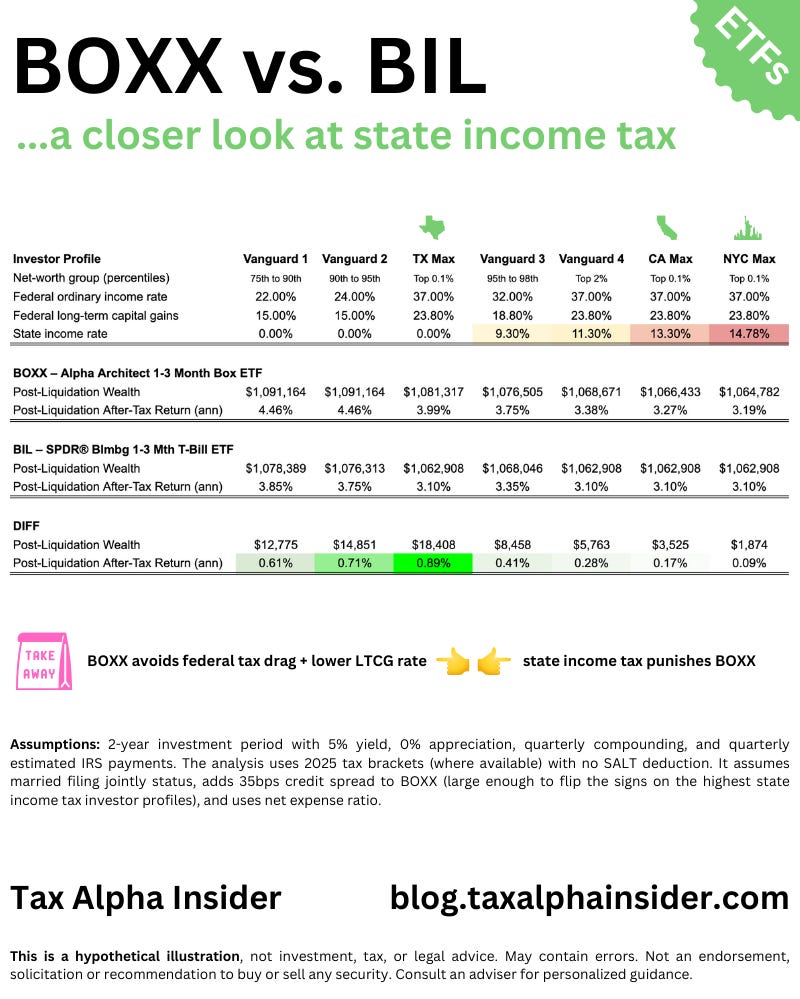

I consider BOXX vs. BIL for seven different investor profiles and a 2-year hold and liquidate strategy to get an apples-to-apples comparison. You can read the assumptions in the infographic for more detail.

Focus on the DIFF section and find Post-Liquidation After-Tax Return (ann). This row tells us if BOXX outperformed BIL on an after-tax basis, and it does in every case.

This depends on prevailing tax rates and my assumption of a 0.35% credit spread between BOXX and BIL, and more stuff. With a smaller spread, BOXX dips below BIL’s post-liquidation performance.

Federal rates

BOXX avoids federal tax drag, so it gets a boost from the compounding but also takes advantage of preferential long-term capital gains rates.

State rates

On the other hand, BOXX is punished by state and local income tax. BOXX is subject to substantial local taxes in, for example, California and New York City, while its traditional competitors are not.

That said, BOXX might be a fine solution for someone while they live in California and know they will relocate to a low/no-tax state like Texas. Then, the investor avoids state tax altogether (investment income usually isn’t subject to California-sourced income policies like Shohei Ohtani’s might be). In this sense, BOXX affords a type of tax planning other similar products can’t.

Step up in basis

I don’t analyze it here, but all of the gains accruing in BOXX could also receive a step-up in basis. Step-up in basis is nearly worthless for BIL since it’s been distributing ordinary income all along.

End

BOXX gives investors a little bit of extra juice for the credit risk it takes. Its unique structure means shareholders will likely have state and local tax due when they eventually dispose of their shares. In some cases, this is minimal; in others, it is a substantial haircut.

There are many more state income tax scenarios to explore. Stay tuned…