When Tax-Loss Harvesting Goes Wrong

Required reading from Kitces Blog

From the Editor

Nearly all research on tax-loss harvesting assumes the highest marginal income and long-term capital gains rates. Only some actually pay these rates. Kitces Blog explores suitability for other brackets, the value of tax-loss harvesting, and when it is not worth the hassle. My goal in highlighting this work is a different perspective on the too-rosy view that all tax-loss harvesting is valuable.

Yet, I have still only scratched the surface. Consumers and their advisers have thoughts on the utility and tradeoffs of adopting direct indexing and tax-loss harvesting beyond the mathematical nuance explored in the following articles. This is a rich topic and an area I am actively researching with polls and dozens of conversations.

Is direct indexing ubiquity inevitable? I’m not so sure.

Tax Tools

Valur: GRAT Calculator

Tax Alpha Weekly

Kitces Blog: Evaluating The Tax Deferral And Tax Bracket Arbitrage Benefits Of Tax-Loss Harvesting

Kitces Blog (Ben Henry-Moreland): Tax-Loss Harvesting Best Practices

Kitces Blog: Is Capital-Loss Harvesting Overvalued?

Kitces Blog (Ben Henry-Moreland): Why Tax-Loss Harvesting During Down Markets Isn’t Always A Good Idea

Leader

In 2014, Kitces looked closely at the value of tax-loss harvesting.

It's crucial to understand cost basis resets lower after harvesting, creating a tax asset now, but increasing future tax liability, all else equal.

EXAMPLE

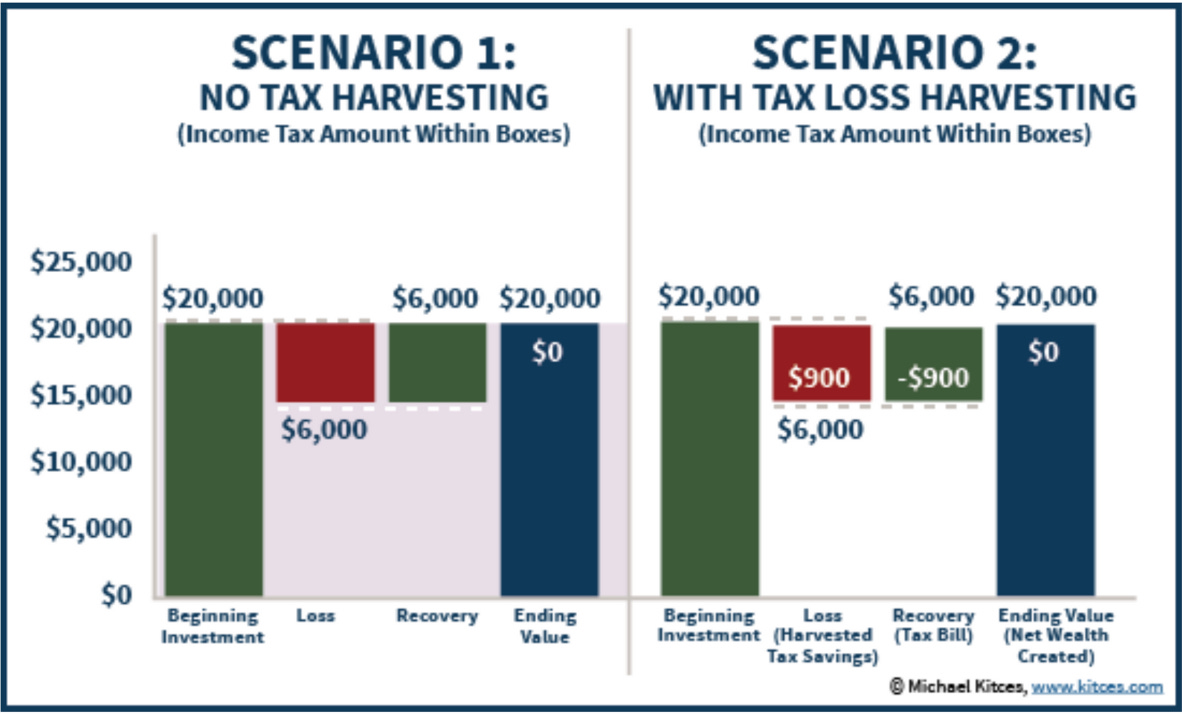

Original investment: $20,000, now worth $14,000 (30% decline)

Harvesting loss generates $6,000 capital loss Tax savings: $900 (at 15% long-term capital gains tax rate)

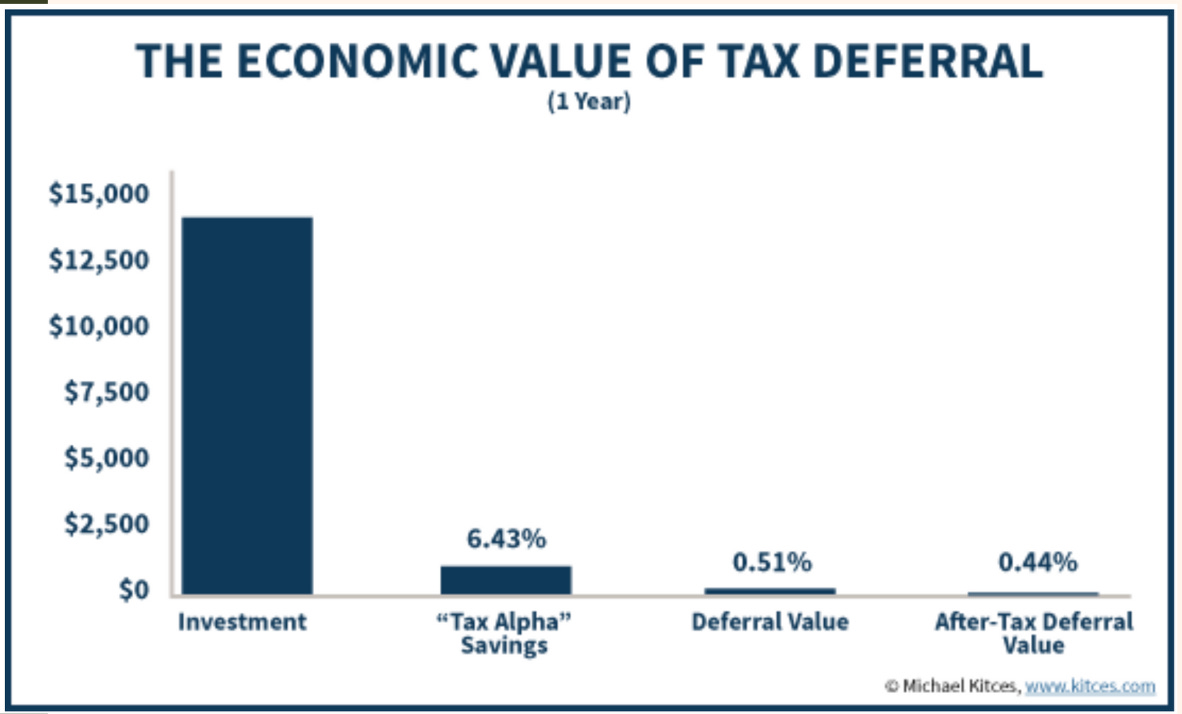

Tax alpha: $900 / $14,000 = 6.4% $900

tax savings invested at 8% return = $72 growth in 1 year

On $14,000 investment, true tax benefit = 0.51%

Net benefit 0.44% after tax on growth

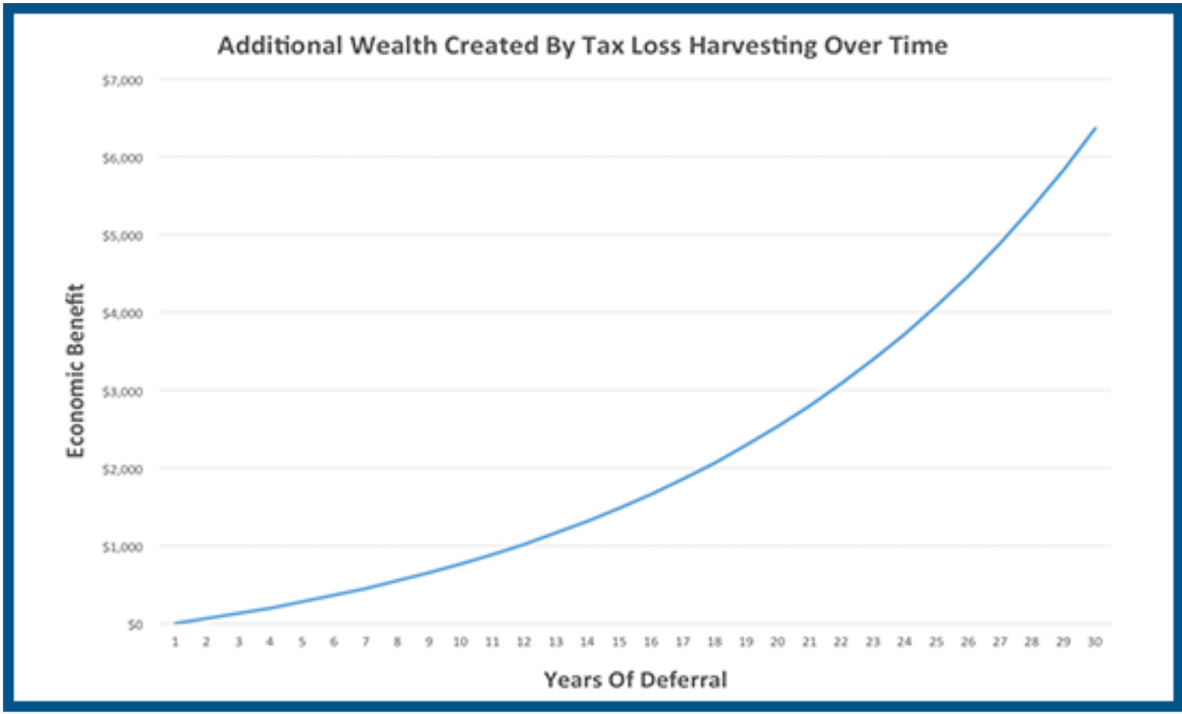

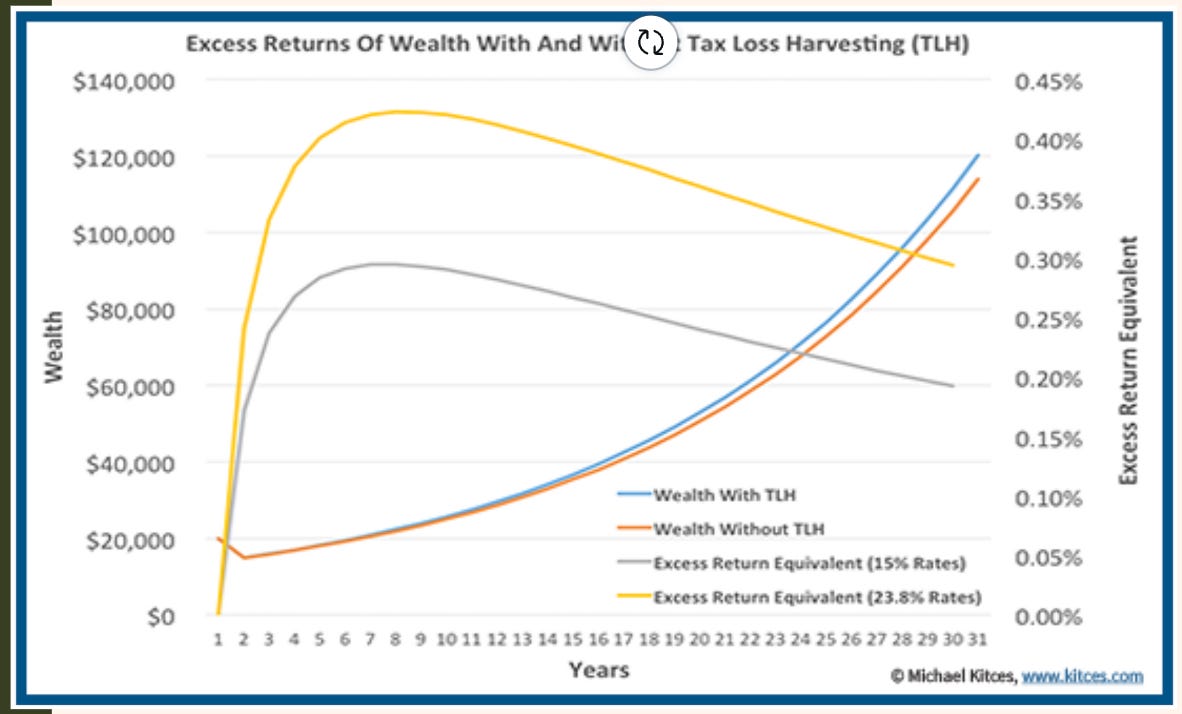

Thus, the benefit of tax loss harvesting over time is effectively a “tailwind” of additional economic growth generated as a result of investing the tax savings from the original harvesting transaction. Kitces (2014)

True benefit = compare wealth created by harvesting vs. not harvesting

Long-term excess wealth compounds, but...

...relative returns flatten after investment recovers above original cost basis

30% decline, 7% growth, 15% tax rate: ~0.30%/year additional annualized return.

Higher benefits at higher tax rates (e.g., 0.42% at 23.8% rate)

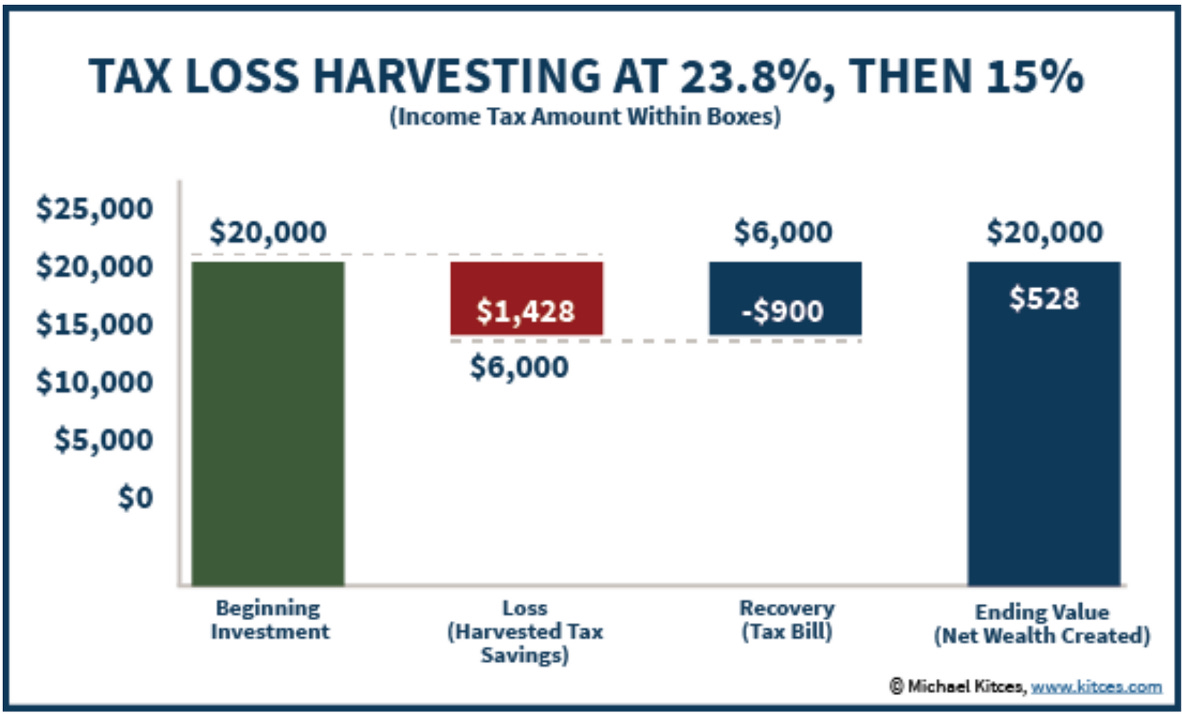

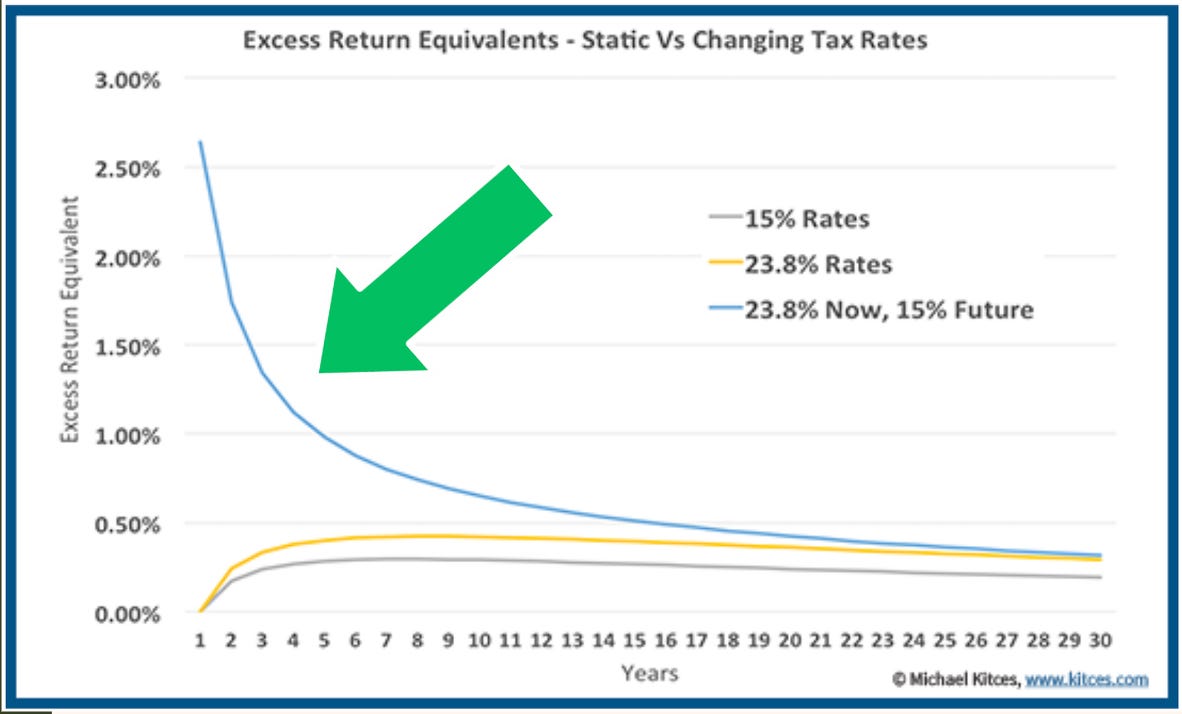

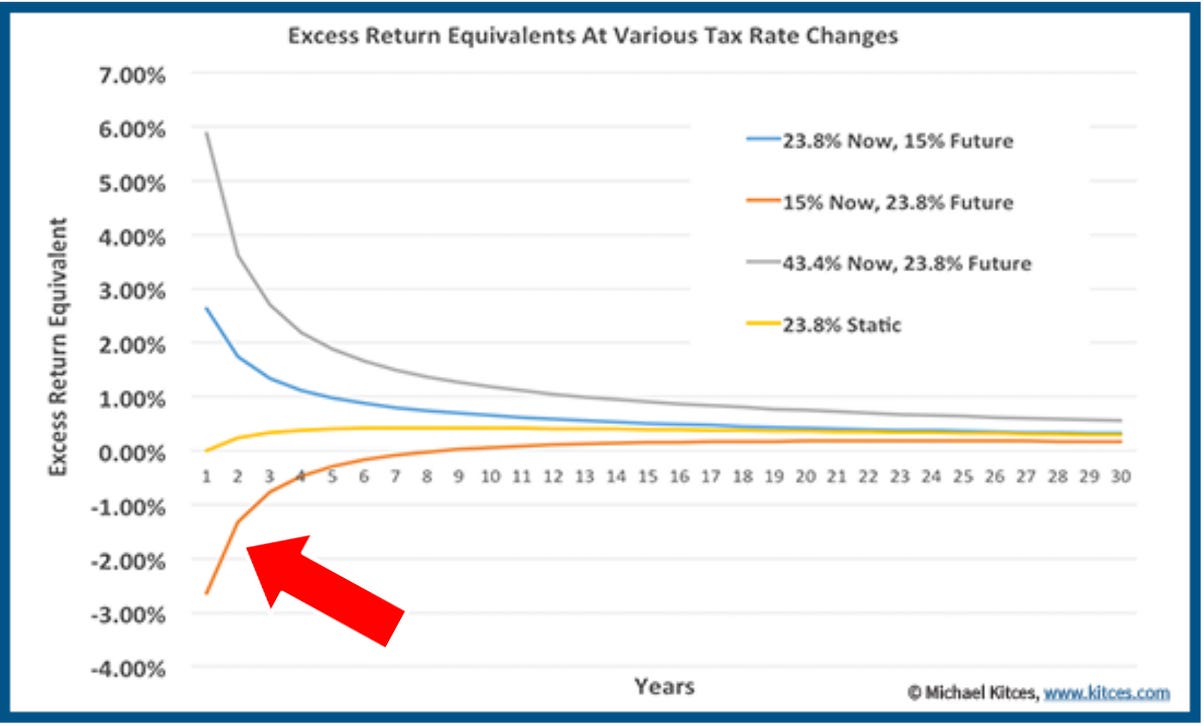

An example of “tax bracket arbitrage”

Current high tax bracket: 23.8% capital gains rate.

Future lower tax bracket (e.g., retirement): 15% capital gains rate.

$6,000 loss: $1,428 tax savings at 23.8% rate.

$6,000 recovery gain: $900 tax at 15% rate.

Net "free" wealth: $1,428 - $900 = $528

The value of tax bracket arbitrage can be substantial... but is rarely mentioned.

Risk of NEGATIVE tax arbitrage ~ “wealth destructive”

EXAMPLE:

Harvesting $50,000/year for 10 years at 15% rates...

Lowers portfolio cost basis by $500,000

Large recovery gain could push investor marginal dollars into 23.8% tax bracket

Future gains taxed at higher rates, reducing overall benefit

When Tax-Loss Harvesting Hurts

Ben Henry-Moreland’s article gives us even more nuance

Net neutral/negative outcomes: Harvesting losses can sometimes leave investors worse off. Specifically…

Higher Future Tax Rates: If future gains are taxed at a higher rate than current losses.

Future Tax Bracket Increase: When additional capital gains push marginal investor dollars into a higher tax bracket.

Unused Carryover Losses: When carryover losses are not utilized before the taxpayer's death.

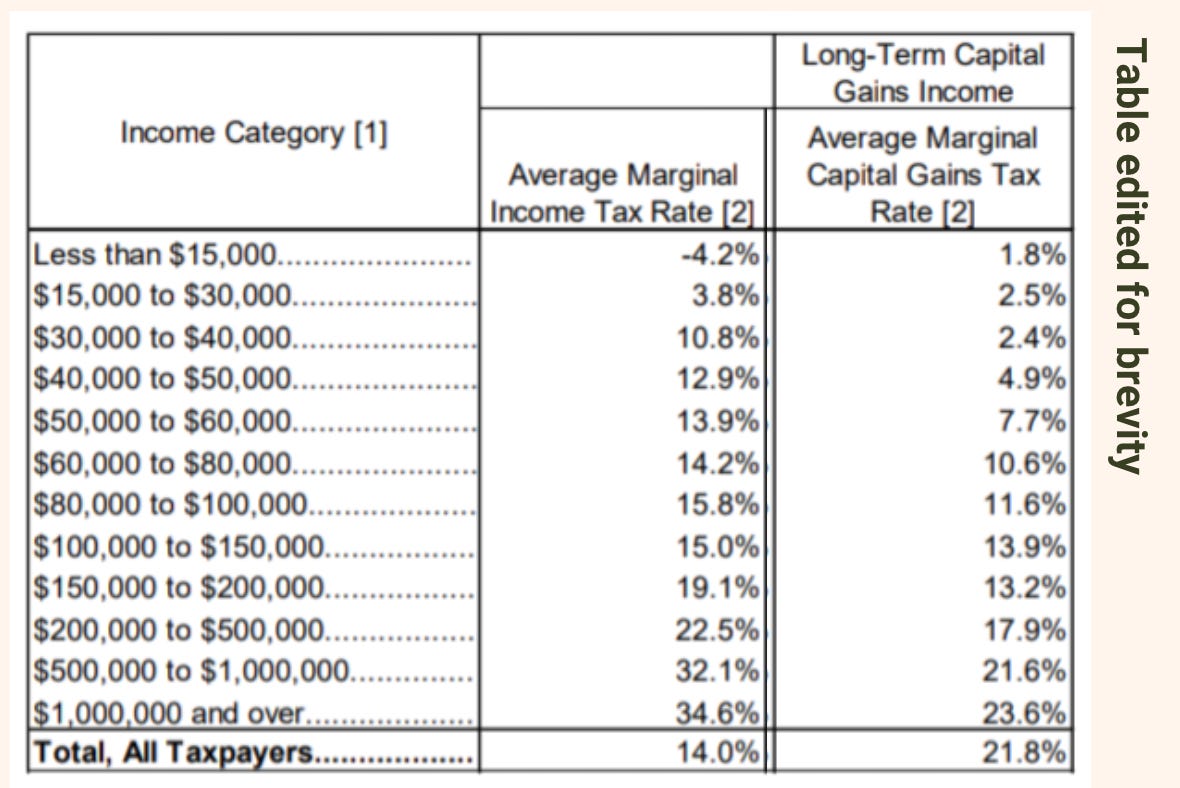

Few Actually Pay The Highest Marginal Rates. We Should Stop Assuming Them

Lastly, Some Food For Thought…

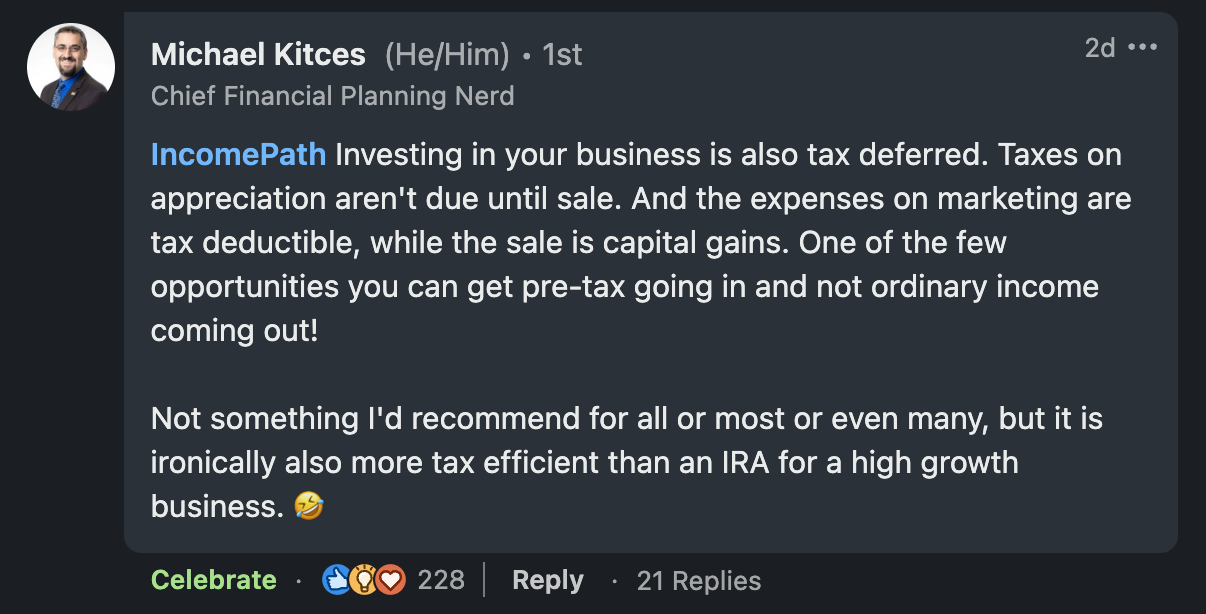

Investing in a high-growth business could be more tax-efficient than an IRA. Pre-tax dollars in and capital gains out. Not bad.