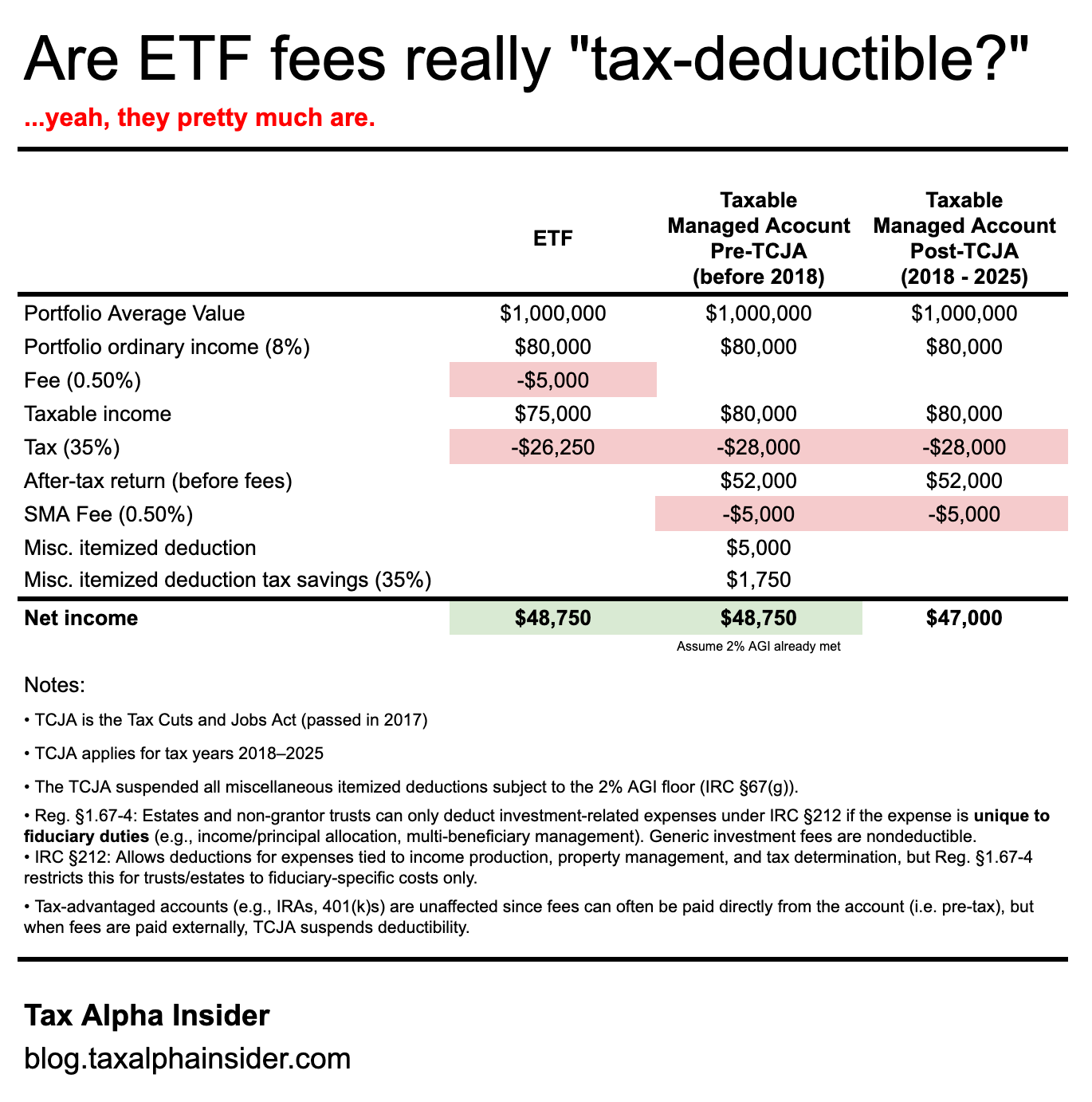

Are ETF fees really "tax-deductible?"

ETF fees are paid pre-tax, while taxable managed account fees are paid post-tax, and are not deductible thanks to the Tax Cuts and Jobs Act (set to expire EOY 2025)

I was flipping through Stuart Lucas’s “The Taxable Investor’s Manifesto” again recently. Near the beginning, he says that “management fees and expenses in mutual funds and ETFs are deductible from profits before calculating taxes.”

Occasionally, folks (usually on the internet) abbreviate this by saying ETF fees are “tax-deductible.” That’s not technically true, but it is a convenient shorthand.

Mutual funds and ETFs subtract fees before making distributions, so deducting them doesn’t make sense.

On the other hand, income from separate accounts is not deductible as of the Tax Cuts and Jobs Act (TCJA) of 2017 (effective 2018 through EOY 2025).

TCJA 2017 suspended all miscellaneous itemized deductions subject to the 2% AGI floor (IRC §67(g)).

Let’s see a toy example…

Hedge fund digression

Hedge fund fee deductibility boils down to distinguishing between "trader" and "investor" funds:

Trader Funds: A trader fund is a hedge fund that engages in substantial, regular, and continuous trading activity with the intent to derive profit from short-term changes in security prices rather than from interest, dividends, or long-term price appreciation. Investors can fully deduct management fees and administrative expenses as business expenses, reported on Schedule E of Form 1040. This requires1:

Trader determination: Based on the fund's trading activity and intent generally toward short-term trading.

Annual designation: A hedge fund declares itself a trader fund retroactively at year-end. This affects the deductibility of fees and tax treatment but not the accounting method.

Section 475(f): Trader funds may elect mark-to-market accounting, recognizing gains and losses as ordinary income, which alters tax treatment and eliminates wash sale rules. This election is distinct and forward-looking.

Investor Funds: Primarily aim to derive profit from interest, dividends, and long-term price appreciation rather than short-term trading. Due to the Tax Cuts and Jobs Act of 2017, investors cannot deduct management fees and administrative expenses through 2025.

Trust and estate digression

The suspension is more nuanced for costs paid or incurred by estates or non-grantor trusts:

IRC §212: Allows deductions for income-producing expenses broadly.

26 CFR §1.67-4: Limits estate/trust deductions to fiduciary-specific costs; routine investment fees are nondeductible.

TCJA Impact: Suspends miscellaneous itemized deductions (2018–2025) for individuals, effectively disallowing most §212 investment-related deductions. However, trusts/estates may still deduct unique fiduciary expenses under §1.67-4. Examples of unique fiduciary expenses:

Income/Principal Allocation: Costs to allocate between income and principal for beneficiaries.

Tax Prep Fees: Preparing fiduciary income tax returns (Form 1041).

Judicial Accountings: Court-mandated fiduciary accountings.

Specialized Investment Advice: Tailored advice for fiduciary-specific needs (e.g., balancing income/growth).

Fiduciary Bond Premiums: Required premiums for fiduciary roles.

Legal Fees: Services tied to fiduciary duties (e.g., trust interpretation, estate settlement).

Retirement account digression

Fee deductibility is nuanced, but the TCJA suspension of itemized deductions primarily affects non-ERISA accounts where external fee payments are possible (e.g., IRAs).

ERISA accounts (e.g. 401(k), 403(b) (non-governmental), and more):

Fee Payment:

Fees are embedded or deducted from plan assets.

Traditional plans: Fees reduce pre-tax account value.

Roth plans: Fees reduce post-tax account value.

External fee payment isn’t allowed, so itemized deduction suspension from TCJA is irrelevant.

IRAs:

Fee Payment:

Fees are usually paid directly from the account:

Traditional IRAs: Fees reduce pre-tax account balance.

Roth IRAs: Fees reduce post-tax account balance.

External fee payment is allowed, but TCJA suspends the deductibility of these expenses (2018-2025).

Bottom line

The takeaway is that ETF fees are paid pre-tax, while taxable managed account fees are paid post-tax (and not deductible). Other vehicles, like partnerships, trusts, and retirement accounts, have additional nuance around fee deductibility.

Is Congress going to allow the TCJA to expire? We’ll see…

Lender Management, LLC v. Commissioner

Relatedly, nerds may be interested in the Lender Management, LLC v. Commissioner case, “which left the US Internal Revenue Service (“IRS”) with the hole in the bagel after it challenged a family office’s position that the costs of running the office were deductible for federal income tax purposes,” wrote Mark Leeds, tax partner with the New York office of Mayer Brown.

This case is a hot topic in family office land since it essentially codifies a playbook for family offices to deduct operating expenses.

That’s an interesting topic for another time.

Until then, thanks for reading.

Sosner, N., & Steblea-Lora, R. (2021). Limitation on trader fund losses under the CARES Act of 2020. The Journal of Wealth Management, 24(3), 2–16. https://doi.org/10.3905/jwm.2021.1.135