Can direct indexing + tax-gain harvesting beat the 529 plan?

Kids qualify for an annual tax benefit that no one uses

– Daniel Gold sent me a message on LinkedIn a few weeks ago with a clever tax strategy for kids. I have two young boys and was curious. Below is his article, with light editing, about direct indexing with tax-gain harvesting applied to the kiddie tax.

Most parents think 529 plans are the best way to save for college. After all, tax-free growth is hard to beat. However, if parents are smart, they can do better than 529s.

If a $10k check is invested for a kid at birth and grows 8% per year, it will be worth ~$50k by the kid’s 21st birthday. A 529 investor would owe $0 on that $40k gain (assuming they use the funds for a qualified educational expense). The strategy below explains how to produce a ~$16k capital loss instead.

1. Understanding the “kiddie tax”

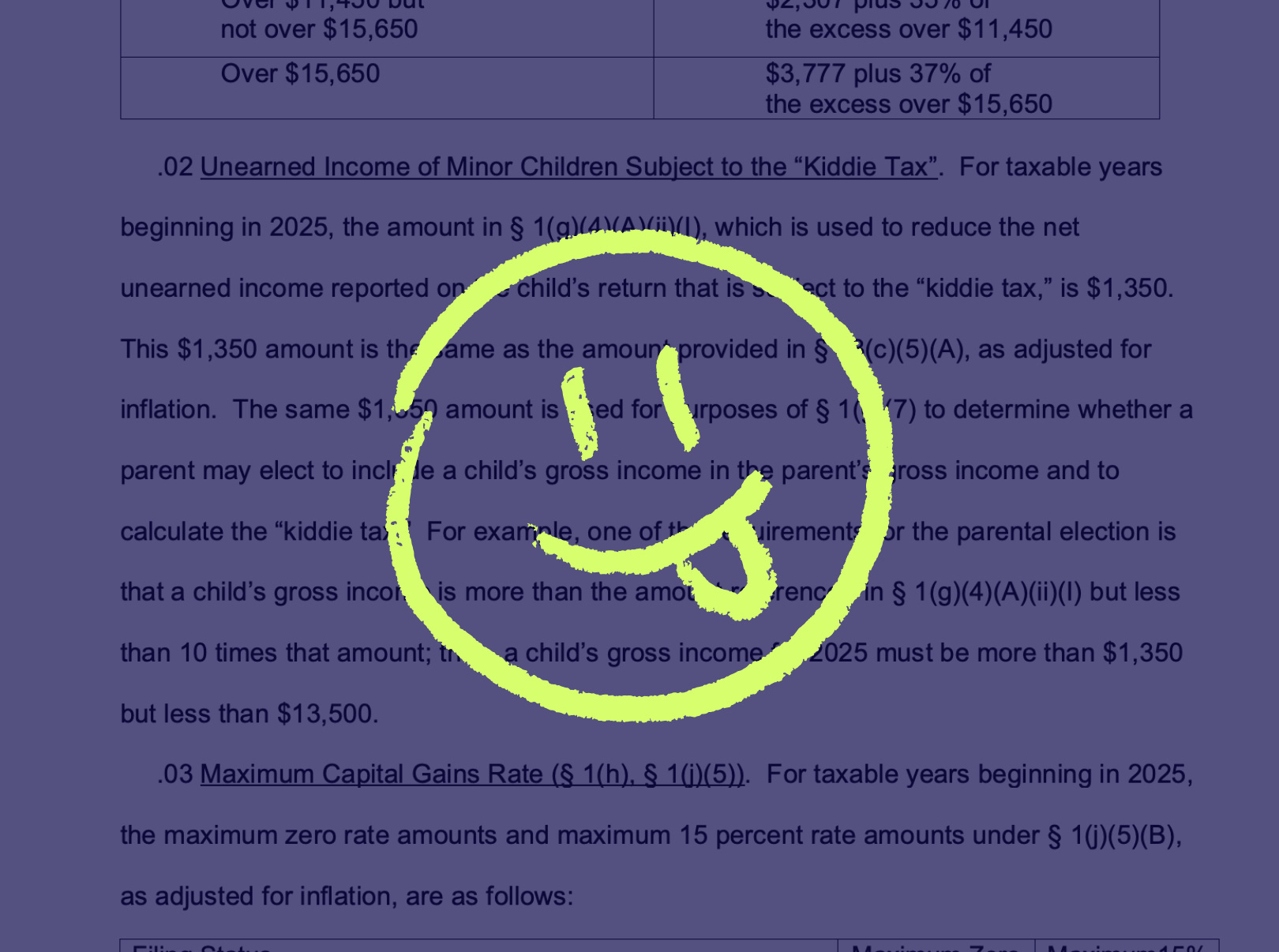

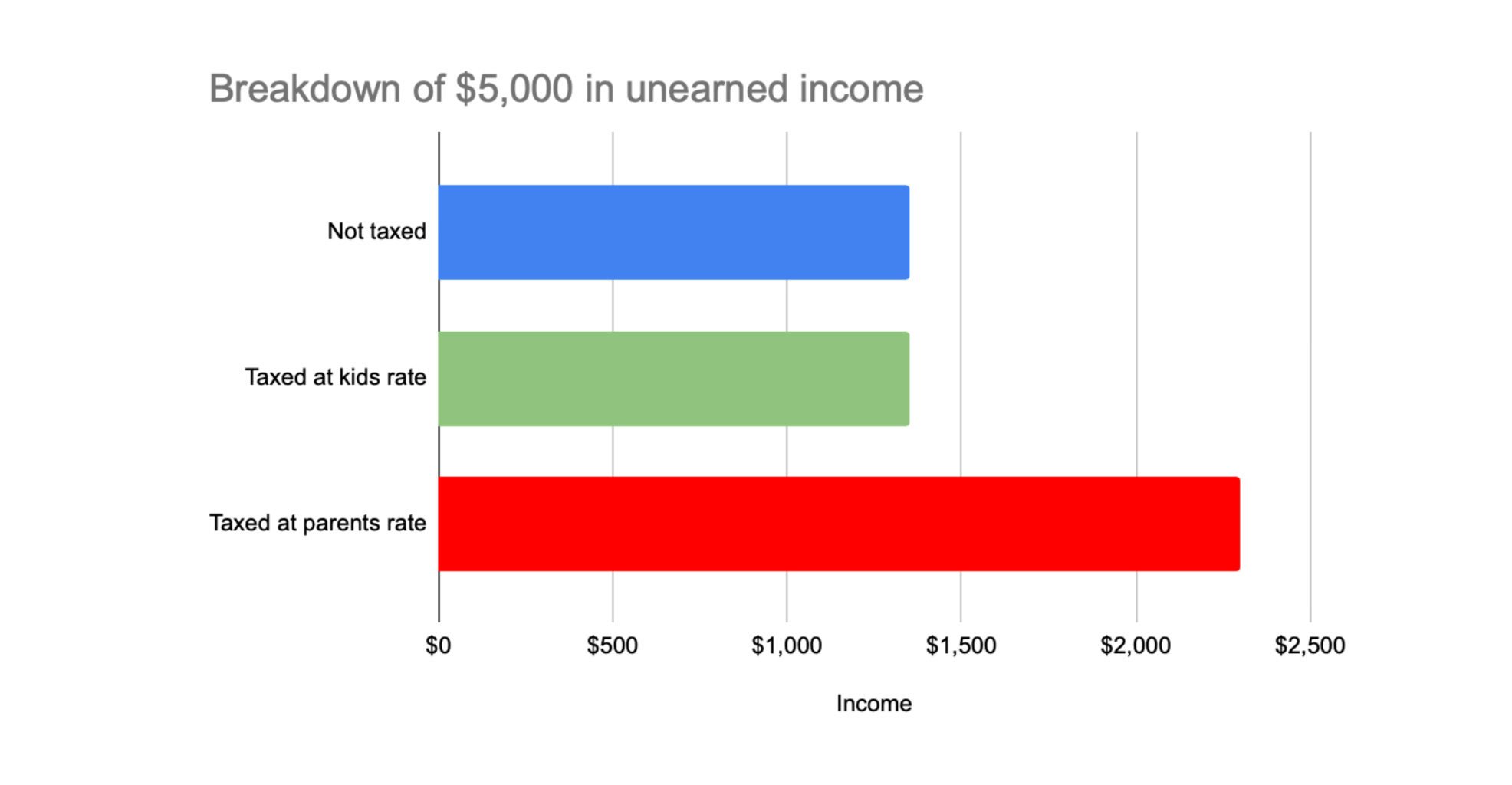

The first $1,350 kids earn in investment income is not taxed. The next $1,350 is taxed at the kid’s rate (usually zero unless the kid has significant earned income). This amount is adjusted for inflation and applies to all investment income, including dividends, long-term capital gains, and short-term capital gains. After reaching the kiddie tax limit, the gains are taxed at the parent's marginal rate.

As long as a kid's income is within the standard deduction ($15,000 for 2025), the true 0% tax amount is $2,700.

The kiddie tax limit applies to any custodial account for a minor's benefit. UTMA and UGMA accounts are the most common examples. These are taxable brokerage accounts controlled by a custodian (usually a parent) for the benefit of a minor. Once the minor reaches the age of majority, which is usually 18 or 21 but varies from state to state, the minor assumes control.

However, before that, the parent can use that money at any time for anything they see fit to benefit the child beyond basic necessities like food, clothing, and shelter.

2. Tax-gain harvesting

Parents should take advantage of the $2.7k limit for their kids every year.

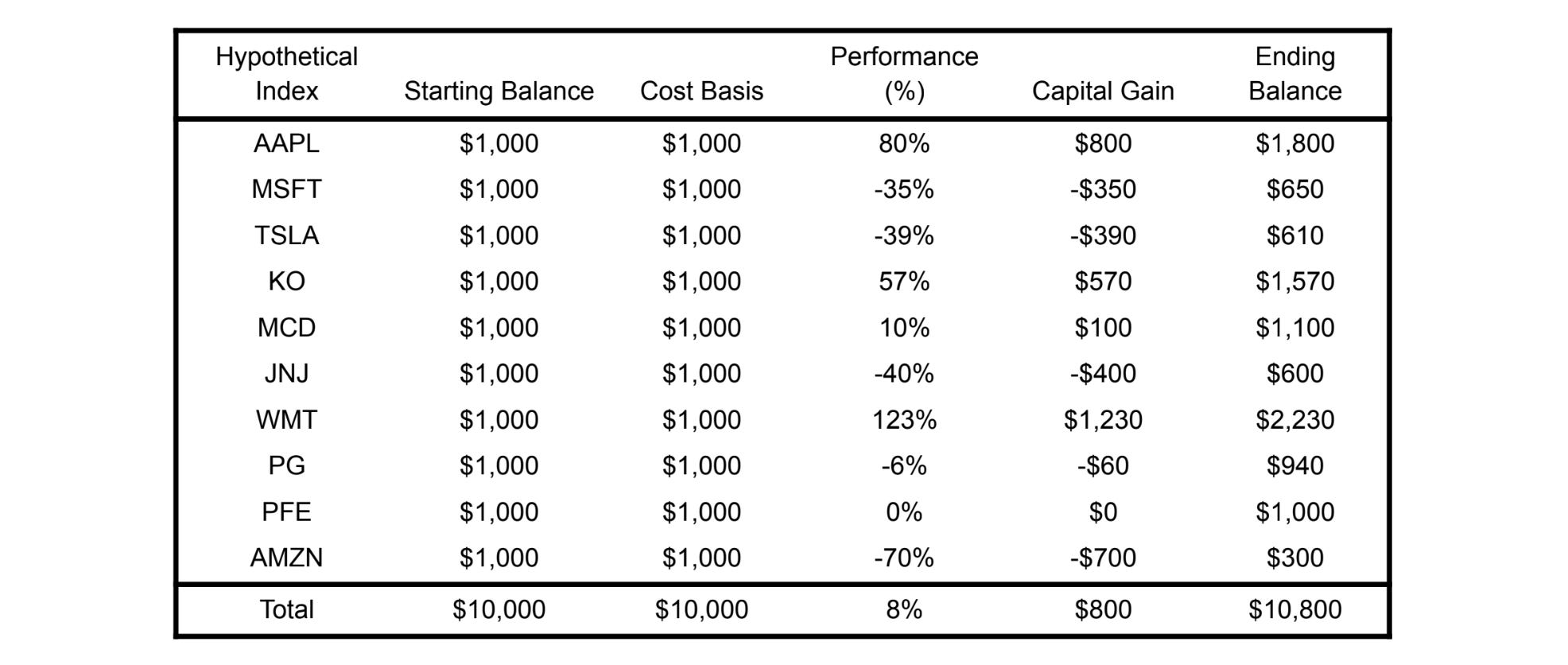

They can do so by selling (and repurchasing) assets at a gain1. This resets the cost-basis higher and means the child may have a loss when they eventually sell the funds. An example of a hypothetical portfolio follows below.

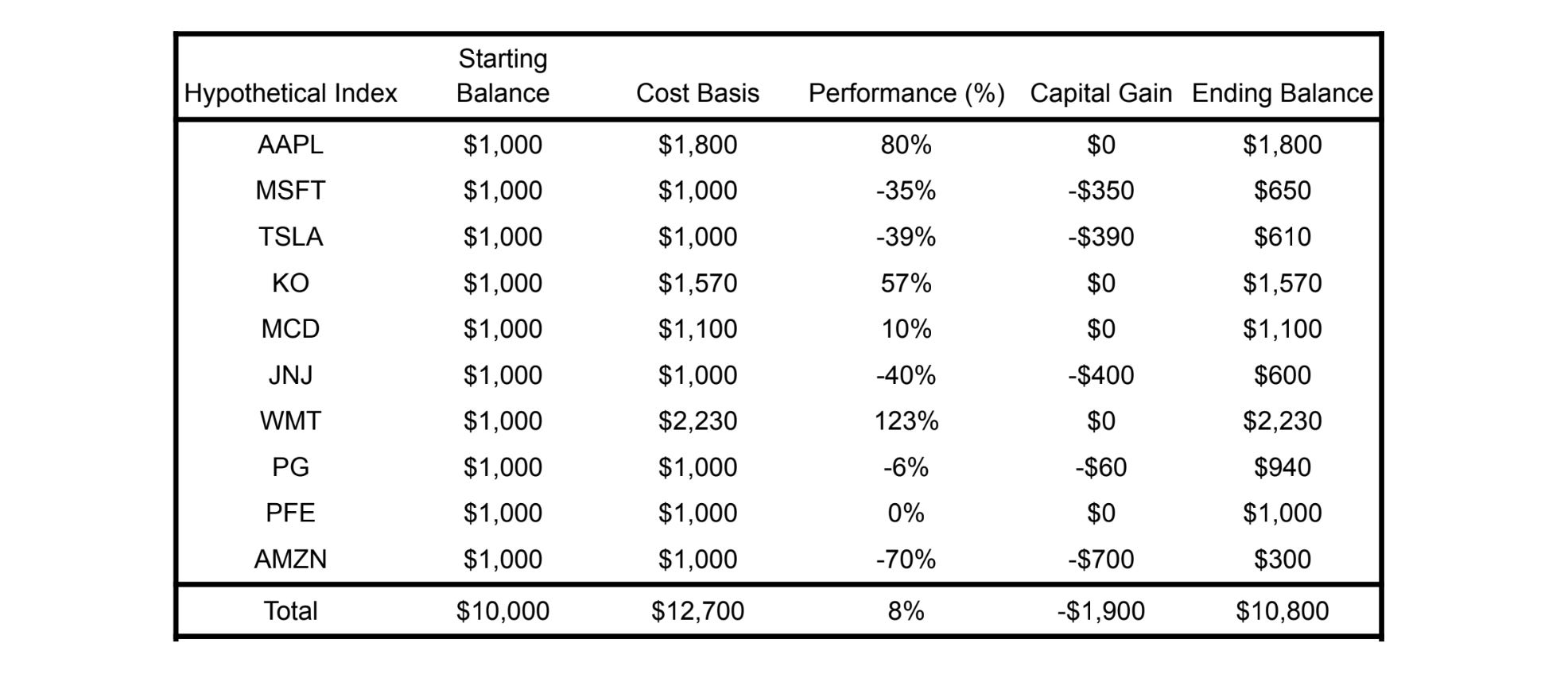

Now imagine you sell AAPL, KO, MCD, and WMT and immediately buy these stocks back. Here is what the resulting portfolio would look like.

Notice that in this example, the kid’s portfolio value is still the same amount, $10,800. The stocks are the same, except the first portfolio has an $800 taxable gain, and the second portfolio has a $1,900 taxable loss. That is the magic of tax gain harvesting.

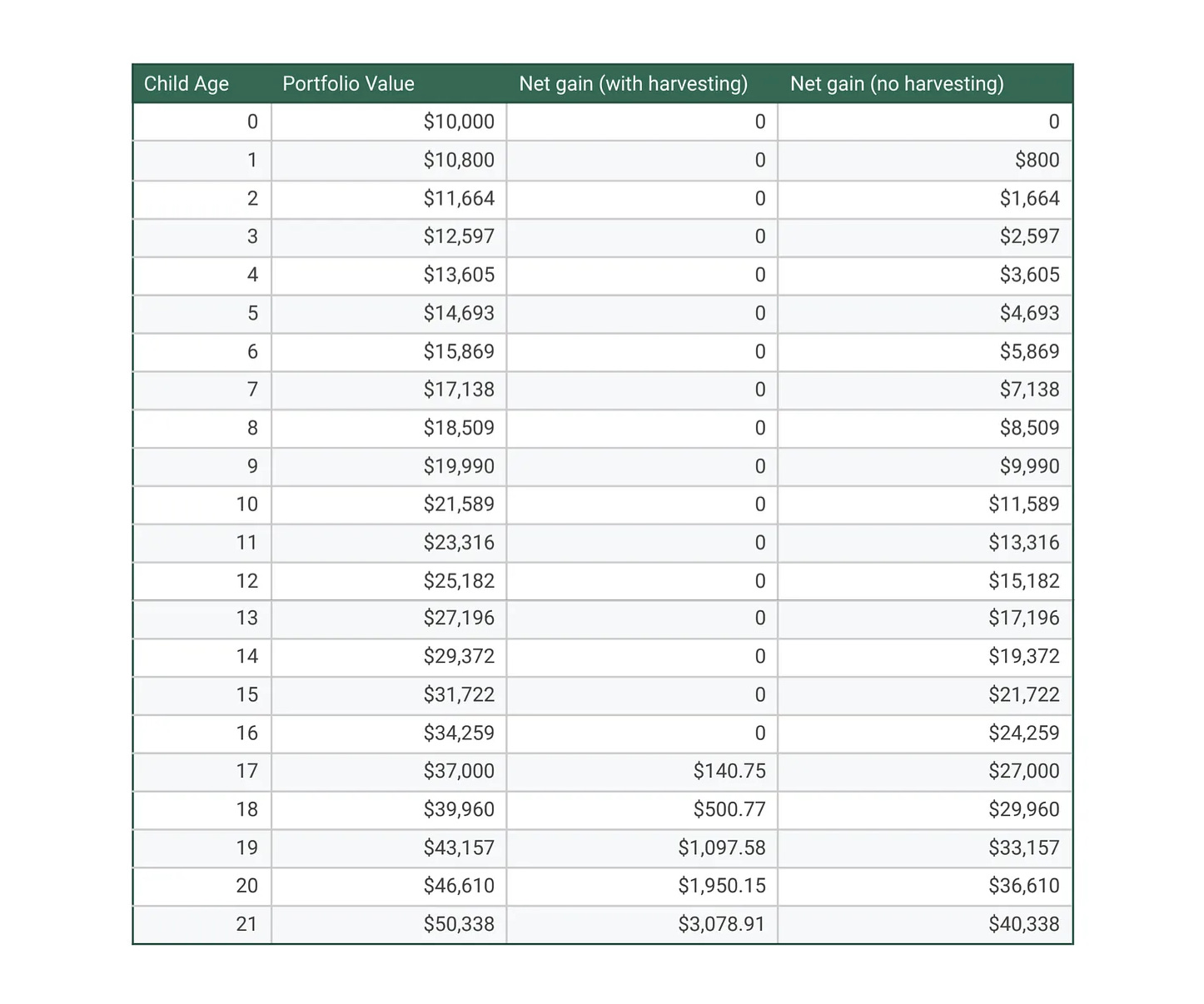

3. $10k invested at a child’s birth

In this example, a parent invests $10k in their child’s account the day they are born. The money grows in an index fund at 8%, leaving the child with ~$50k on their 21st birthday. Typically, this would be a ~$40k gain, but with systematic gains harvesting, the child would only have a ~$3k gain. The strategy entails selling and buying back the most appreciated ETFs to use up the annual $2.7k limit.

4. Direct indexing

In the above example, the child “wastes” some of their annual limit most years.

For example, the portfolio is up by $800 in year one. All gains have been realized, but $1.9k remains in the 0% bracket that is not being utilized. Even at larger portfolio values, ETFs run this risk—if the market is down, there could be no gains to realize.

When you sell an ETF, you sell some stocks at a gain and some at a loss. Direct indexing has gained popularity because it allows investors to target the losses in a portfolio to sell. On the other hand, it also allows you to target the gains. Fractional share trading means direct indexing could be applied in this strategy.

Direct indexing replaces a sledgehammer with a scalpel.

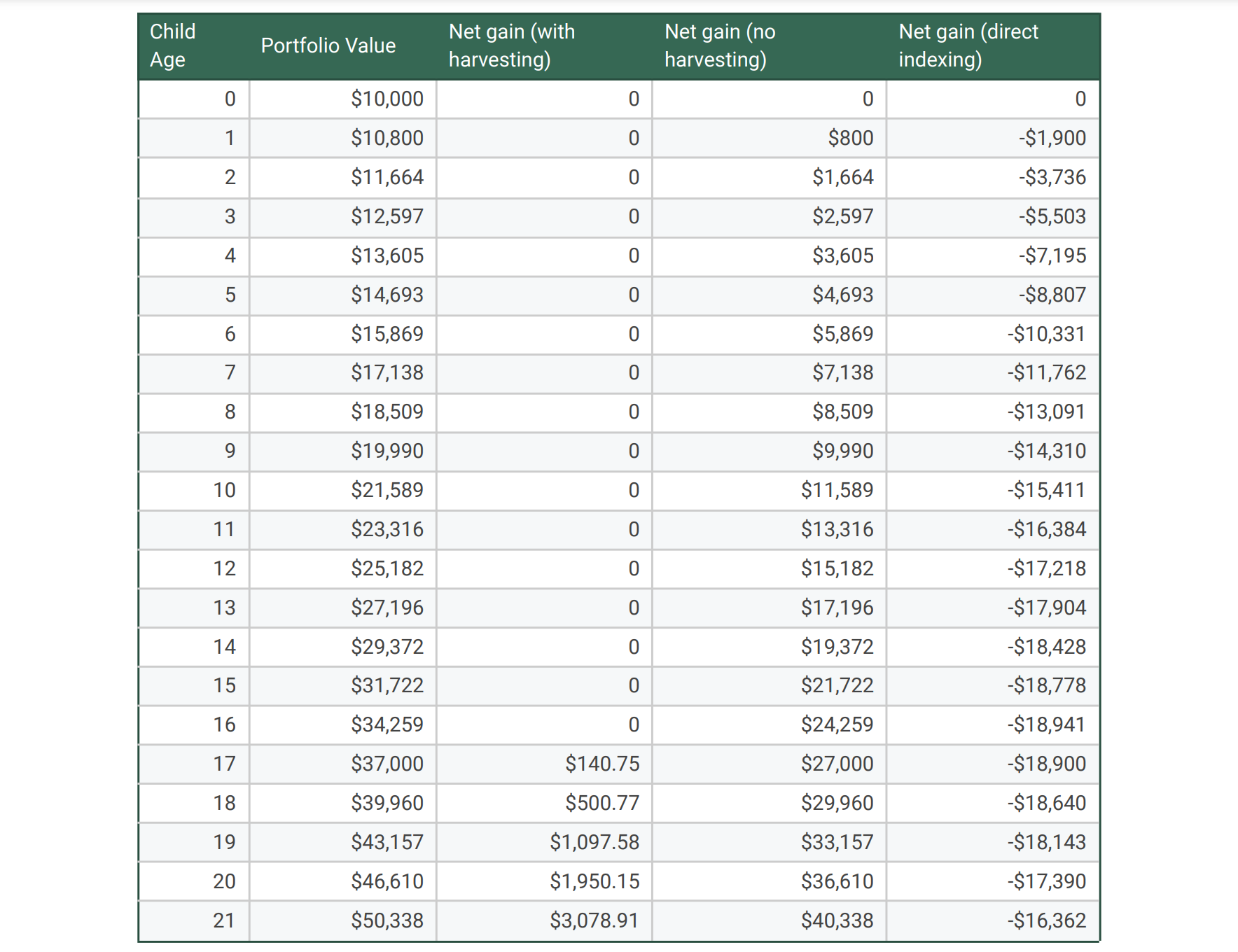

An ETF up 8% may be one basket of stocks down 15% and another up 31%. In that case, you can sell the stocks at a gain to take full advantage of the kiddie tax limit, leaving behind stocks at a loss for the child to harvest when they turn 21 (assuming the losses stay losses).

The following table illustrates this hypothetical scenario: direct indexing targets $2,700 in realized yearly gains.

The child saves over $19k in capital gains by direct indexing compared to ETF gains harvesting.

It is important to note that when tax-loss harvesting is used, the benefit of direct indexing is that taxes are deferred.

The benefit of tax gain harvesting is that taxes are eliminated by taking advantage of the annual kiddie tax limit.

The child could exit the direct index at any time, and they would still have $19k less in capital gains. You have permanently reset their cost basis $19k higher.

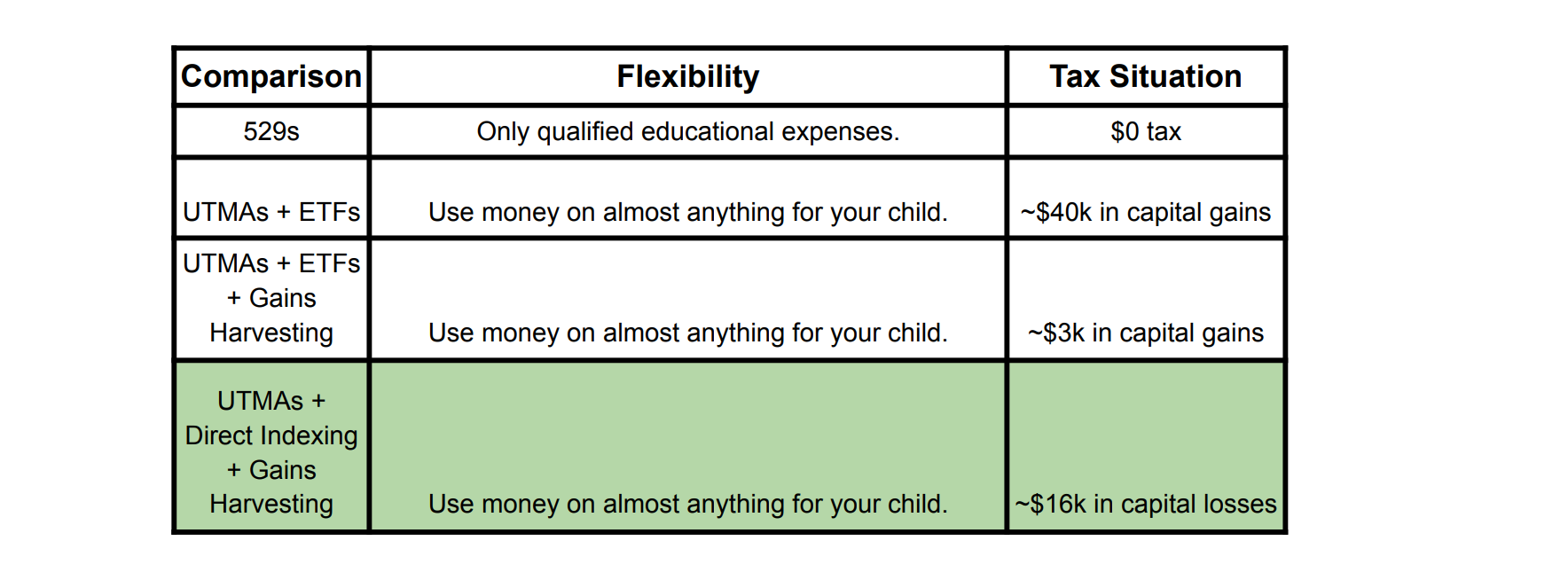

The chart below compares the four options discussed above.

5. Does this scale?

No, this doesn’t really scale. If your portfolio is too large, you’ll get more gains than you can harvest. If the portfolio goes up $3k but can only harvest $2.7k, you’re better off just being in a 529. This suggests that a gain harvesting strategy and a 529 plan may complement each other.

If saving $100k for college, the first $10k might be more tax-efficiently invested with systematic gains harvesting. The remaining $90k could then go into a 529 plan.

Even at small dollars, the value here can still be significant for two reasons:

First, the first $3k in annual tax losses are most valuable because they offset ordinary income. If a minor generates $16k in losses, that's 5 years where they can offset $3k in income (again, assuming losses stay losses).

Second, this is a great way to protect against overfunding a 529. Funding a 529 properly requires a guess about how the market will perform, and if the market does better, you can wind up overfunded. Your child may want to use the remaining funds for a down payment on an apartment or a first car out of college, but they can’t. This strategy gives parents and their kids additional breathing room and optionality.

6. How can I do this?

Bright Path Portfolios is building the first-ever direct-indexing algorithm for kids. Contact Daniel Gold (daniel@brightpathportfolios.com) to join the waitlist or learn more. The first 10 people or advisors joining the waitlist get 50% off management fees for their children or clients.

Disclaimer: This article is for general education and research purposes. It is not investment advice or a recommendation to buy or sell any security. It is not an endorsement of any investment product or strategy. Investors should speak with a qualified adviser for personalized guidance and check with tax counsel about any changes to the Internal Revenue Code.

The wash sale rule applies to realized losses, not realized gains