Can I diversify a large single-stock holding tax-free by seeding an ETF in-kind?

No. Section 351 tests for diversification at the individual and aggregate levels.

I get a lot of questions about why an investor might seed an ETF in-kind, and the mechanics of the Section 351 conversion.

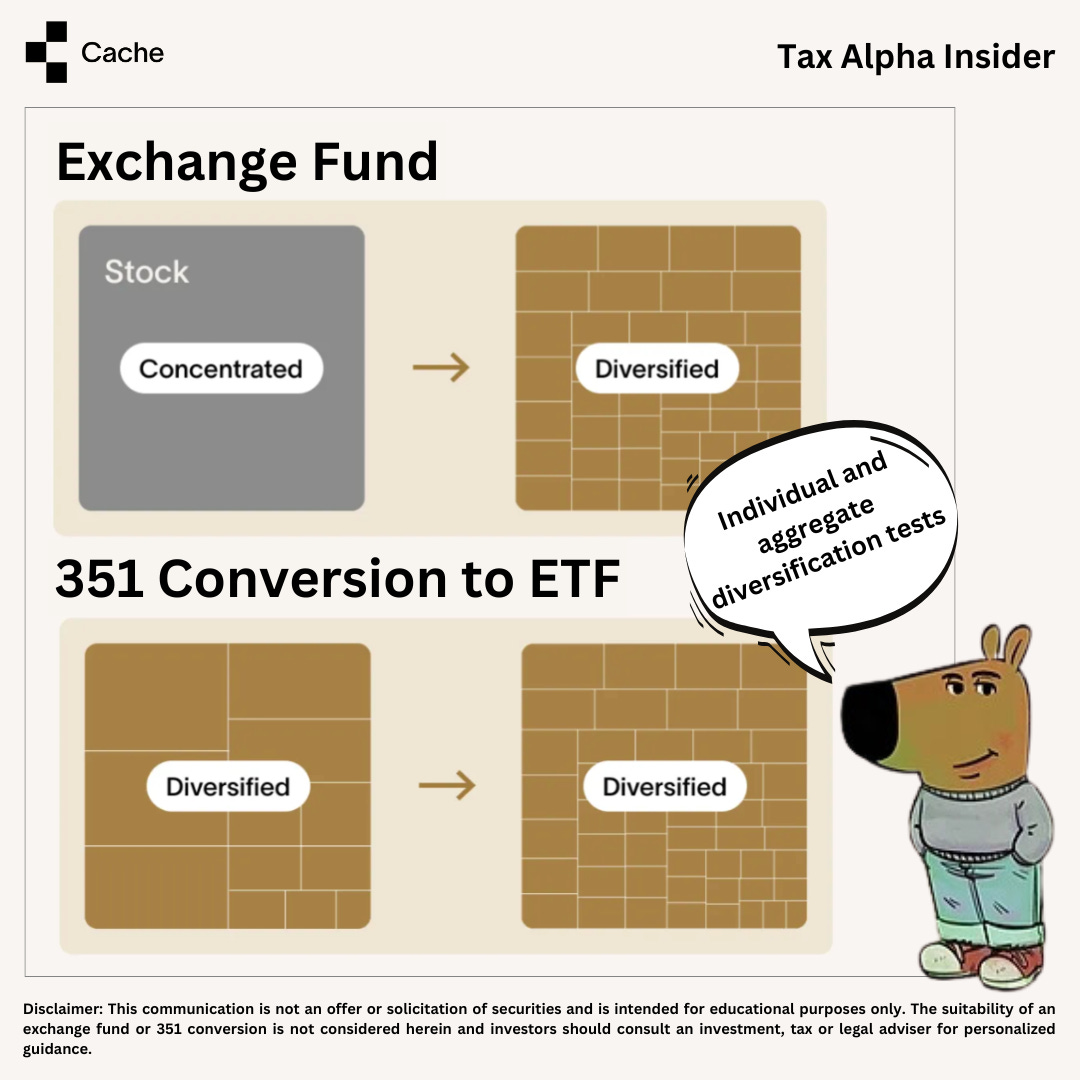

ETFs offer potentially lower costs, broader investment selection, and heartbeat trade tax efficiency.

Section 351 conversion allows investors to contribute diversified assets in a one-time, pre-launch window without immediate tax consequences.

What the FAQ?

The most common question people ask me about Section 351 is: Can I seed an ETF in-kind with mutual fund shares? (answer: technically yes, practically no)

The next most common question is…

Can I diversify a large single-stock holding tax-free by seeding an ETF?

The answer is no.

Section 351 has a diversification test for each transferor and the aggregate fund.

The diversification test

Section 351(e) explicitly denies tax-free treatment if the transfer results in diversifying the transferor's interests.

What is “diversification? Here is Section 351’s two-part test to check if assets are already diversified.

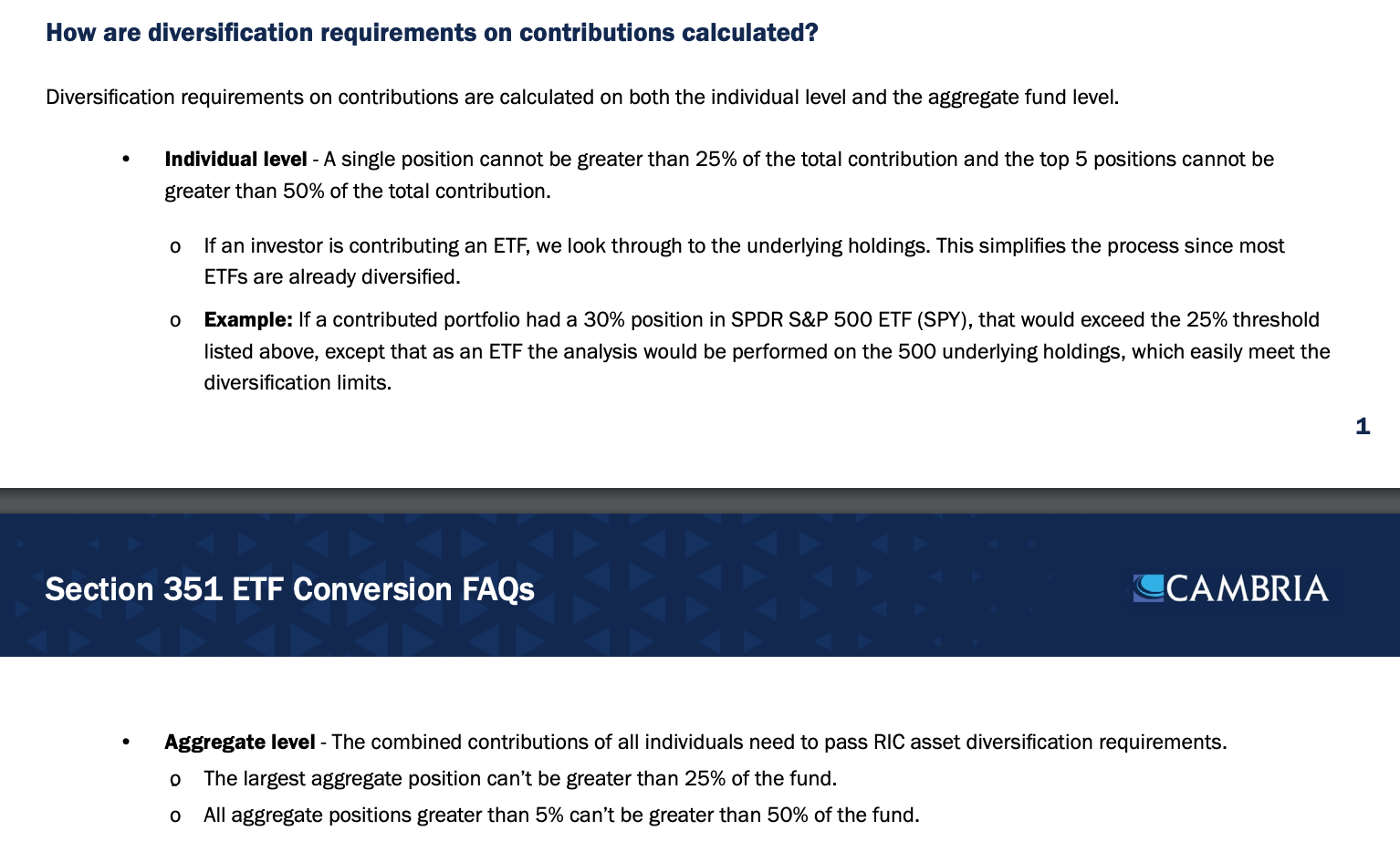

25% Limit: No more than 25% of the total portfolio value can be in securities from any issuer.

50% Limit: No more than 50% of the portfolio value can come from securities of five or fewer issuers.

(Cash and government securities are excluded from diversification calculations)

What about a collection of single-stock positions?

What if 100 investors pooled their single stocks, and the combined result met the section 351 definition of “diversified?”

In this scenario, the concentrated investors achieve diversification, which means they recognize a gain.

The New York State Bar Association Tax Section wrote in Report No. 1252 (2011) that tax-free diversification would violate the intent of Section 351 conversion…

The investment company provisions were enacted decades ago to eliminate taxpayers’ ability to use the tax-free provisions of the Code to diversify appreciated positions in investment assets without the recognition of gain.

Here’s an interesting worked example from Treasury showing that the aggregate portfolio is tested for diversification, wrecking a tax-free transfer.

Example 2. A, together with 50 other transferors, organizes a corporation with 100 shares of stock. A transfers $10,000 worth of stock in corporation X, listed on the New York Stock Exchange, in exchange for 50 shares of stock. Each of the other 50 transferors transfers $200 worth of readily marketable securities in corporations other than X in exchange for one share of stock. In determining whether or not diversification has occurred, all transfers will be taken into account. Therefore, diversification is present, and gain or loss will be recognized.

(emphasis is mine)

And here’s Cambria with some explicit wording on individual and aggregate-level diversification testing.

Side note: Notice mention of the SPDR S&P 500 ETF (SPY) receiving look-through treatment under the diversification tests. We’ll examine the implications another time.

For reference, here’s a deep comparison of Section 351 conversion and the exchange fund.

Investors and advisers must look elsewhere for solutions to a single-stock concentration problem.

p.s. TAX, seeded in-kind via Section 351, launches tomorrow. Expect a recap in your inbox Thursday morning.

Disclaimer: None of this is an investment, tax, or legal advice. It may contain errors (though I try my best). This is not an endorsement of any security, investment product, or company offering such products. Investors should consult with licensed professionals for personalized guidance.