ETFs Could Soon Bail SMAs Out of Lockup

The §351 conversion allows investors to seed new ETFs in-kind

Meb Faber announced a new ETF recently called Cambria Tax Aware ETF. Its ticker?

TAX.

“If you truly understand the implications, this should be a tectonic shift for the asset management industry.”

He’s not talking about some new portfolio tax strategy. He’s talking about normalizing §351 conversions, which allow investors to contribute assets in-kind to an ETF. By contributing assets in-kind, TAX shareholders avoid realizing capital gains en route to investing in TAX.

Wes Gray, CEO & Co-CIO of Alpha Architect, explains it this way…

“The most exciting opportunity in the [now $10 trillion] ETF space is the tax-free conversion from traditional asset wrappers—such as mutual funds, hedge funds, and separately managed accounts (SMAs)—into ETFs. It’s like upgrading from a vintage car to a high-performance vehicle, but without the tax bill.”

The §351 conversion makes sense when investors and their advisers can streamline operations, access new investment vehicles, and simply do better using the ETF wrapper. Tax deferral happens to be a (very powerful) side effect.

A get-out-of-jail-free card

ETFs are ridiculously tax-efficient.

Separately managed accounts (SMA) have advantages, but they lose their charm when a portfolio grows well above cost basis. Tax-loss harvesting becomes less likely, and rebalancing requires realizing more capital gains.

The SMA portfolio becomes "locked up." 🔐

What if SMA investors could rebalance without paying tax now? That's what ETFs do (via in-kind redemption).

If investors could in-kind their SMA into an ETF, once there, the ETF could rebalance the locked-up assets without immediate tax consequences. This is what Cambria's TAX unlocks.

From the press release: "TAX allows individual investors to seed the launch of the ETF with their separate account investments."

A §351 conversion is how this happens. It is a get-out-of-jail-free card, effectively freeing assets from locked-up SMAs without any present tax implications.

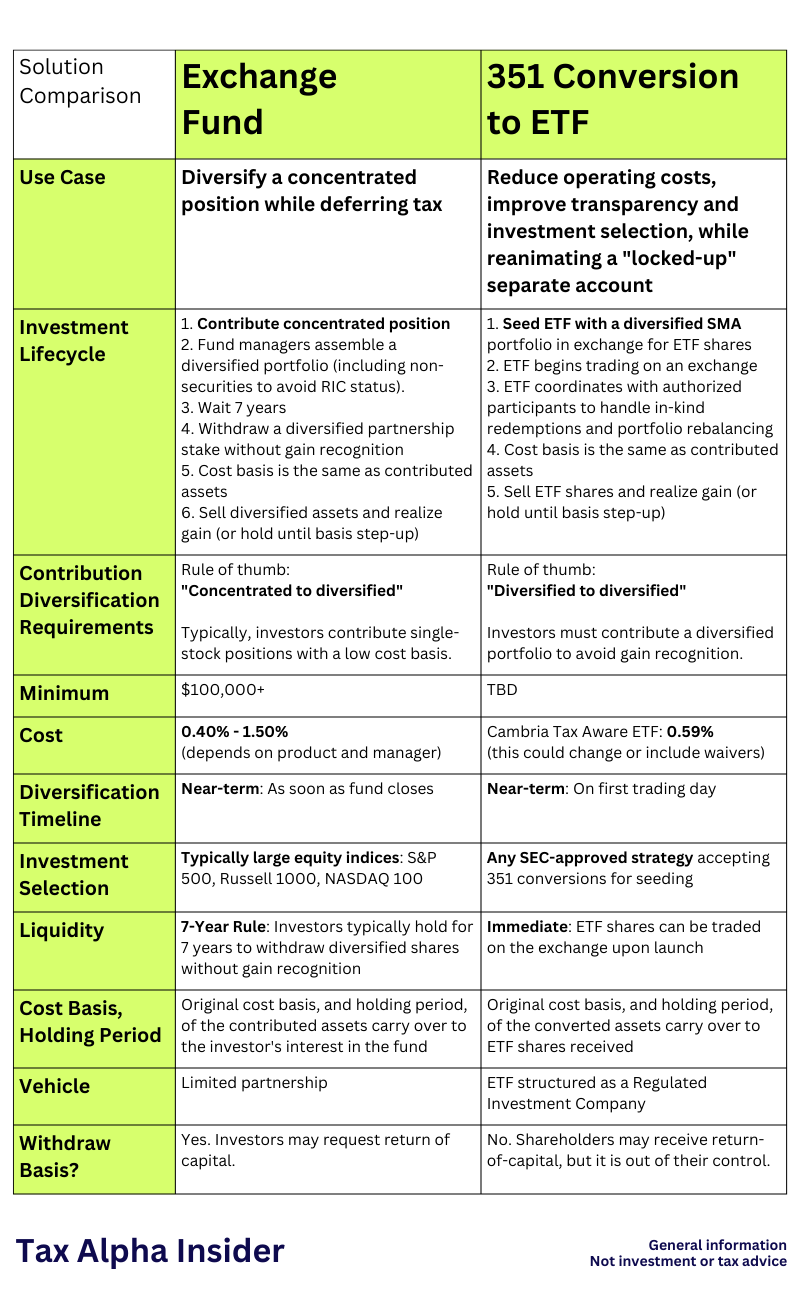

Is the §351 conversion the same as an exchange fund?

No.

Several folks compared the §351 conversion to an exchange fund, but these solutions solve very different problems. Depending on an investor’s circumstances, some combination of exchange fund and §351 conversion could make sense.

The difference is first the use case, but perhaps equally important, the diversification rules.

Here is a point-by-point comparison.

How does the §351 conversion work?

The mechanics of a §351 conversion are horribly boring. You can read about them here.

From an investor’s perspective, every step in the process matters, but counsel paid by the ETF sponsor will mostly handle it.

However, investors and allocators should study closely the composition of the assets that will move from SMA to ETF.

At first glance, transferring separate account assets to regulated investment companies (like ETFs) is excluded.

"...IRS does not want parties to be able to make non-taxable transfers to an investment company unless the portfolio being transferred to the ETF is already reasonably well-diversified," writes Bob Elwood in ETF Architect's document attached to the TAX request for info.

All investors need to do is check some diversification boxes (per Treasury Regulation Section 1.351-1(c)(6)) and a few other boxes. Come to think of it, the ETF needs to check some boxes, too, but assuming satisfactory all-around box-checking, the §351 conversion works.

The crucial detail is that the §351 conversion cannot achieve (or plan to achieve) portfolio diversification.

Diversification

The diversification tests can be found in 368(a)(2)(F)(ii)1, and it’s important to know you can’t game them2.

From Cambria’s whitepaper on §351 conversions:

No single holding can exceed 25% of the total portfolio.

Holdings over 5% cannot collectively exceed 50% of the portfolio's net asset value.

"Look-through" applies to regulated investment companies and REITs.

Helpfully, Cambria simplifies the tests into simple examples:

Qualifies [for §351 conversion]:

20% Nvidia and 80% assorted stocks (1% each).

100% SPY ETF.

A 10-20 stock portfolio, roughly equally weighted.

Does Not Qualify:

50% Nvidia stock and 50% cash.

A portfolio of mutual funds.

A portfolio of Dogecoin.

Assuming diversification does not result (or plan to result…) from the conversion, and all other boxes are checked, the assets can transfer to the regulated investment company without immediate tax implications, and investors get their ETF shares (and collectively have “control”).

Tax avoidance?

Investors and advisers have practical reasons to convert using §351, including consolidating operations to reduce costs, portfolio transparency, access to more sophisticated instruments, and more.

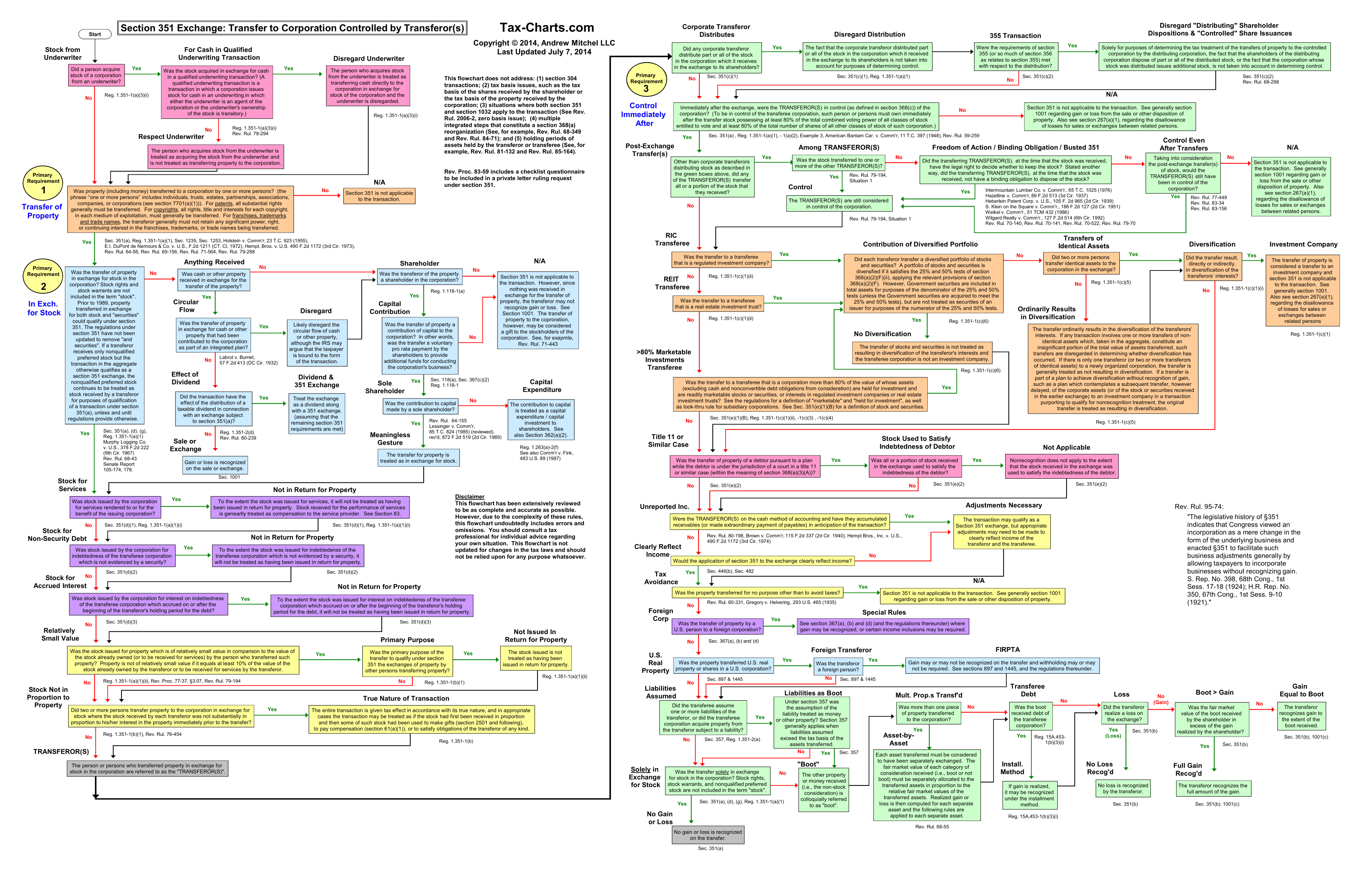

Interestingly, someone created a flowchart for a §351 conversion. If you zoom in, it includes fascinating detail.

One case stuck out to me. In Gregory v. Helvering (1935), the Supreme Court ruled that a taxpayer’s use of a new corporation to transfer shares and reduce taxes wasn't valid. Even though the taxpayer followed the rules, the Court found the transaction was only meant to avoid taxes. The taxpayer had to pay the tax.

The point is that tax efficiency is a powerful perk but not the primary or sole reason for the conversion.

Why now?

The "tectonic" shift Meb referred to is not just TAX, but a conveyor belt of ETFs:

• Seeded in-kind.

• Managing a different strategy.

• Opening a new seed/in-kind window.

• Acting as get-out-of-jail-free card for another batch of locked-up SMAs.

"Cambria plans to follow TAX with a series of ETFs open to all investors and seeded with individual separate account contributions." (from the PR)

That's tectonic.

More questions than answers

What is special about this moment that allows Cambria to reimagine how ETFs are seeded?

Is the §351 conversion somehow cheaper than ever before?

Why now?

Why aren’t all ETFs funded in-kind?

I don’t have answers yet, but there’s a chance I will soon.

For now, the takeaway is that TAX could catalyze a trend, but it’s unclear why ETF sponsors with 1,000x the resources haven’t already done so.

Why actively managed?

TAX is supposed to launch in December. I have a few mechanical questions about the §351 conversion, but they are minor. I suspect details about the §351 conversion won’t kill the deal for anyone (unless they’re confused about the diversification rules).

My guess is that the fees and active strategy could kill the deal for some.

I chatted with an adviser recently who told me they’re uncomfortable with the 0.59% expense ratio.

So, I followed up with the folks at ETF Architect and confirmed that the law firm working on the 351 conversion will be paid by the ETF sponsor, not by shareholders.

Moreover, TAX’s “Fees and Expenses” table says that all 0.59% is “Management Fee", which investor.gov defines as “A fee paid out of fund assets to the fund's investment adviser for investment portfolio management.”

So, I think it’s fair to conclude the 0.59% expense ratio, which is 100% management fee, does not directly include costs associated with the 351 conversion.

The point is that investors are not directly paying for the §351 conversion, so what are they paying for?

What do investors get for 0.59%?

The principal investment strategy from the October 1, 2024 prospectus reads:

“Utilizing its own quantitative model, the Fund’s investment sub-adviser, Cambria Investment Management, L.P. (“Cambria” or the “Sub-Adviser”) selects value stocks with lower dividend distributions, which are generally taxed as ordinary income.“

This may just be an odd word choice, but TAX’s universe, “the largest 1,000 U.S. equities by market capitalization…,” generally pays qualified dividends, which are not taxed as ordinary income. Perhaps they’re talking about screening names that pay non-qualified dividends?

Later, the prospectus says nearly the same thing again: “The Fund will invest in stocks that have lower dividend distributions, which are generally taxed as ordinary income.”

What does “lower dividend distributions, which are generally taxed as ordinary income” mean?

In any case, the general strategy seems to be: “Cambria screens out high dividend yielding stocks and selects companies with strong value metrics to optimize the Fund’s after-tax returns and reduce investors’ tax liability associated with dividend distributions.”

From a tax perspective, reducing dividends is sensible. Back in 2018, Rob Arnott, sorta the OG of taxable investing, wrote in Is Your Alpha Big Enough to Cover Its Taxes? A 25 Year Retrospective that “The tax burden can be reduced by… reducing dividend yield.”

However, Arnott also wrote “Active managers still have a hard time consistently generating pre-tax alpha, and the fees of active managers are still high.”

That was 2018, and TAX didn’t exist back then, but still, making the case for active in mid to large-cap stocks seems tough nowadays.

One reason for including the active bets is the Economic Substance Doctrine, but that’s a topic for another time.

What are the tradeoffs?

TAX is an actively managed ETF, first and foremost driven by stock-picking. Part of the strategy is identifying value, which is somehow related to minimizing dividend yield, which has some tax advantages. In-kind contributions (a one-time event) are a substantial perk but not the main event of (ongoing, billed) portfolio management.

To put this in perspective, the iShares Russell 1000 Value ETF (0.19% expense ratio, and an index-tracker according to its prospectus, and also 0.40% cheaper than TAX) as a rough proxy for TAX’s investment universe, has a trailing 12-month yield of around 1.82% (Sept. 30, 2024). If I assume all income from the fund comes from dividends and apply the maximum qualified dividend rate of 23.8% (again, for ballparking), I see 0.43% in tax savings annually from side-stepping dividends.

This isn’t perfect and ignores any pre-tax complications, portfolio growth, changes in dividend yield, personal tax brackets, state/local tax, and more, but it gives me a sense of where shareholder money is going.

In this case, it seems like 0.43% saved tax on dividends goes to Cambria in the form of a 0.40% higher fee (beyond the iShares index tracker).

Very roughly, my intuition is that the iShares product and TAX are basically equivalent on an after-fee, after-tax basis, so my remaining question is…

Is Cambria’s active stock selection worth the price?

Of course, it’s hard to ask and answer this question in isolation. The option to fund the ETF in-kind via §351 conversion is valuable.

Investors, therefore, need to consider whether the 0.59% expense ratio and the uncertainty of active selection are reasonable costs for the operational and tax advantages TAX offers. For the right investor, they could be.

References

ETF Architect. Introduction to ETF Taxation and 351 Conversions. Havertown, PA: ETF Architect. Retrieved from https://www.etfarchitect.com

Scarpa, C. C., & LaFalce, R. C. (2015). Thinking about Converting to a RIC? Important Considerations. Presented by Stradley Ronon Stevens & Young, LLP.

“A corporation meets the requirements of this clause if not more than 25 percent of the value of its total assets is invested in the stock and securities of any one issuer, and not more than 50 percent of the value of its total assets is invested in the stock and securities of 5 or fewer issuers…”

From Scarpa (2015): “If a transfer is part of a plan to achieve diversification without recognition of gain, such as a plan which contemplates a subsequent transfer, however delayed, of the corporate assets (or of the stock or securities received in the earlier exchange) to an investment company in a transaction purporting to qualify for nonrecognition treatment, the original transfer will be treated as resulting in diversification.”

Very thorough information here on the 351 Conversion process. Thanks. If anyone wants to participate in a conversion they can get matched up with ETF launches here https://351conversion.com/