Options-Powered ETFs: Democratizers & Disruptors

New strategies and revamped old ones, all powered by options and delivered in the ETF wrapper, will change how we think about investing... if we can grok them

In late 2019, the SEC adopted The ETF Rule, 6c-11 exemptive relief.

This replaced the lengthy regulatory review each ETF endured with a simpler, standardized process. Before 6c-11, options gummed up the process. After, the floodgates burst open.

Two types of ETFs, both innovative and powered by options, emerged:

The Disruptors, and…

The Democratizers

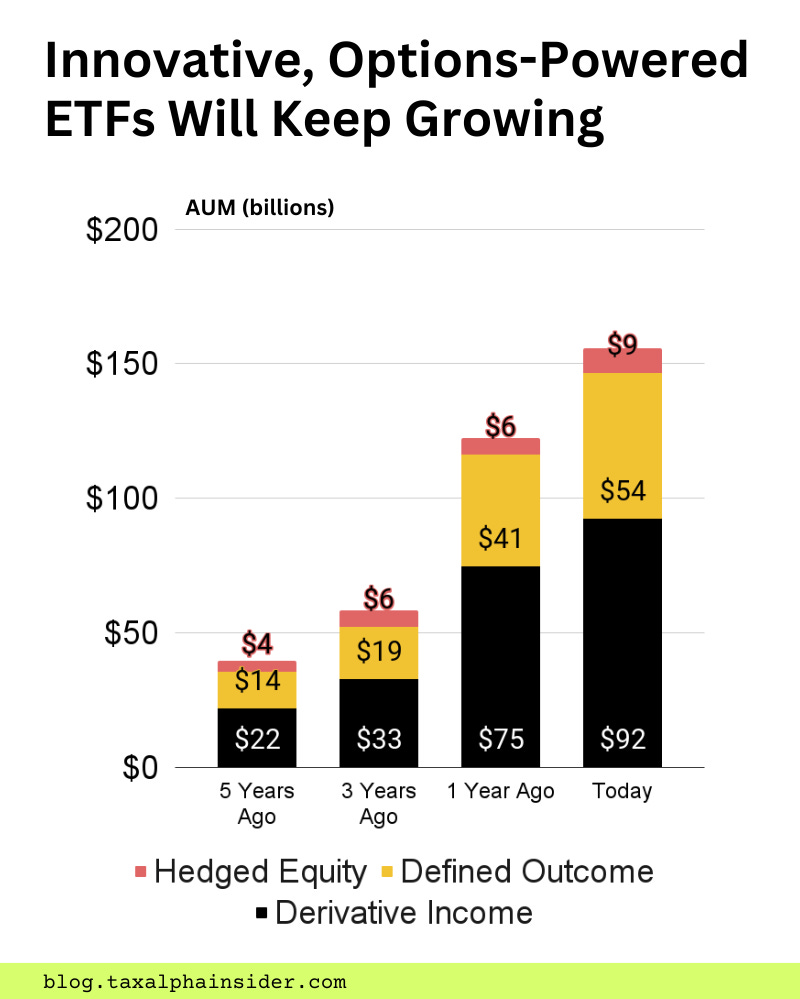

The Democratizers

Since 6c-11, new ETFs have included riffs on covered calls, tail hedging, relative value, buffer, and more. These products make sophisticated strategies accessible or introduce new strategies designed to take advantage of the ETF wrapper. They democratize fancy stuff for the rest of us.

Collectively, the Democratizers amount to more than $150 billion AUM (up more than $100 billion over the last 5 years).

Buffer ETFs (which I always mistype as “bugger”) are still in their infancy, though they have enormous promise in risk/reward management and tax efficiency. They deserve a closer look.

The Disruptors

The other flavor of options-powered ETF is the Disruptor.

It includes BOXX, Alpha Architect’s box spread ETF, and Twin Oak’s Short Horizon Absolute Return ETF (TOAK). Both are actively managed and seek returns similar to short-dated bonds. They disrupt our notion of an asset class. “Do we need bonds?” they seem to imply.

Options, plus the active mandate, give portfolio managers the flexibility to adjust implementation details and generate active returns. Plus, they leverage a deep and centralized options market.

They are also taxed differently than short-dated bonds. In particular, options-based strategies generate capital gains rather than ordinary income (generally a good thing for investors, all else equal).

Options are also redeemable in-kind, meaning shareholders can likely defer tax on their investment, in some cases, indefinitely.

One caveat is that options are taxed federally and locally, while Treasury bonds are only taxed federally, and muni bonds are only occasionally taxed locally (more on this another time).

As a case study, the following table shows BOXX ETF versus the ultrashort bond category (TOAK is relatively new and does not have a Tax Cost Ratio as of this writing).

BOXX is very tax efficient compared to its peer group.

Side note: Tax Cost Ratio does not include state and local tax or post-liquidation tax (e.g. capital gains due upon selling the ETF), so it is an imperfect, but still reasonable, metric for understanding tax efficiency. I wrote a whole article about it.

Side note: I’m investigating BOXX and expect to write about it before the end of 2024

The Disruptors depend on put-call parity to deliver familiar risk and reward with, at times, far superior tax efficiency1.

Landmines

The Democratizers and the Disruptors will change how we think about investing…if we can grok them.

While no one is replacing their very-cost-and-tax-efficient Vanguard equity ETFs, they may add hedging or market-neutral strategies or more tax-efficient versions of fixed income, to name a few possibilities.

The trouble for taxable investors (and wholesalers) will be explaining what's happening inside the ETF wrapper. This matters for due diligence.

If I had to summarize due diligence, I would say investors want to know:

What they are buying

What could go wrong

Whether it’s a good deal

Complexity will push many investors away. Though some will take a leap of faith and trust their wholesaler, only a few will understand what’s happening inside the wrapper.

Sussing out “Whether it’s a good deal” could mean quantifying the overall cost of the ETF by summing the expense ratio and the total tax expense. This would help investors avoid stepping on tax landmines.

A landmine is when an ETF sponsor delivers a shiny, new product with reasonable pricing but extreme tax inefficiency. These products really annoy me. And I’m glad to say I am actively working on quantifying their total cost for all to see.

Until then, investors need to do their own research. Those who do may find a new product that solves their exact problem, or they may avoid stepping on a landmine. In either case, ETFs are changing, and options will play a bigger role.

Disclaimer: This article is for general educational and journalistic purposes; it does not constitute investment, tax, or legal advice. This is not an endorsement or recommendation to buy, sell, or transact any investment product.

For an interesting read on this, see Warren, Alvin C. 2004. “US Income Taxation” of New Financial Products.” Journal of Public” Economics 88 (5): 899–923. https://doi.org/10.1016/S0047-2727(03)00042-2.