Tax Deferral Is The Hottest Thing In ETFs?

Tax efficiency won't drive the next $10 trillion in ETF AUM... well, maybe it could.

Or… send me an idea directly…

Last week, I spoke with seven ETF sponsors about the future of ETF tax efficiency.

The future of ETF tax efficiency might be the future of ETFs.

Themes from the discussions:

Only a small subset investors and advisers see tax as a portfolio cost on par with fees and commissions (evidence: tons of mutual funds paying insane distributions and AUM still growing).

Many ETF sponsors see capturing AUM from mutual funds (not other ETFs) as the largest opportunity.

Many ETFs are “naturally” tax efficient (examples: some US tech and healthcare equity ETFs pay no dividends and don’t trade), while some are “naturally” tax-inefficient (examples: most bond ETFs).

A tiny subset of ETF sponsors (maybe 10-20 of the 400+) are actively working to make their products even more tax-efficient. (send me a message with your favorite so they are on my radar!)

The most compelling innovations in ETF tax efficiency deliver expected risk/return but defer or eliminate income from bonds and dividends.

While the world is pining for income for covered call ETFs, the tax-efficient community is deferring income.

I’ll have more to say about this through the end of the year. I’ve previously called this category of ETF sponsors the Disruptors.

There’s another big trend in ETF tax efficiency worth noting…

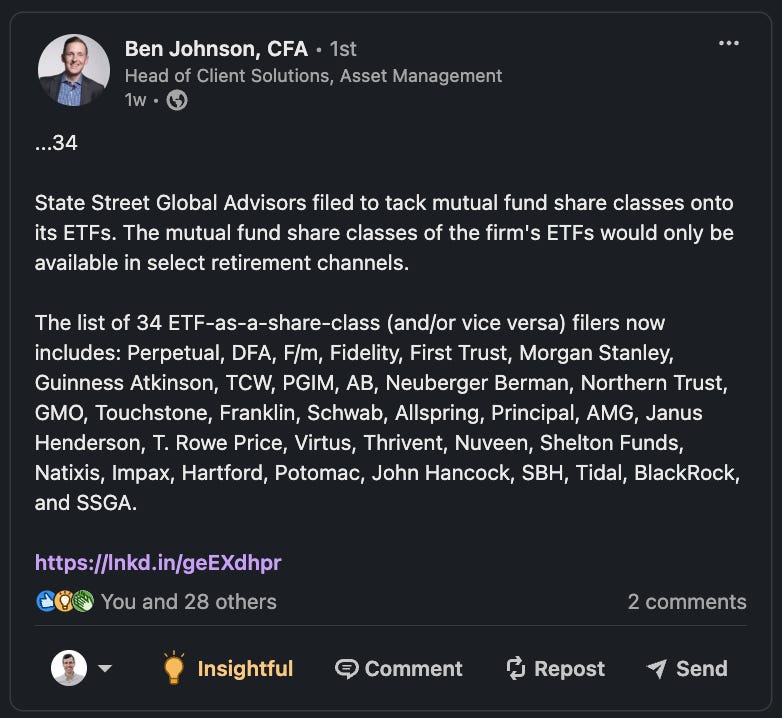

ETF Share Classes

Many mutual funds are petitioning to add an ETF share class. Decades ago, Vanguard established (and patented) this pattern and has since used it in so-called heartbeat trades, which have the net effect of allowing ETFs to avoid distributing capital gains and, therefore, enable indefinite tax deferral.

The patent, although dubiously defensible, expired in 2023, and now everyone wants in.

Most of Ben’s posts have a handy link, so we can look at one petition right now…

This all began with the Vanguard Exemptive Orders (2000-2007):

SEC allowed Vanguard to offer index-based funds with mutual fund and ETF classes.

Expanded relief included domestic equity, international equity, and bond index funds.

…and continued with 6c-11 (2019):

Provided general exemptive relief for ETFs but excluded ETF classes combined with mutual fund classes.

SEC’s concern was apparently different transaction methods (in-kind for ETFs vs. cash for mutual funds), which would increase costs for all shareholders.

What’s happening now:

Funds must apply for exemptive relief on a case-by-case basis.

What’s new?

Allow funds to offer ETF and mutual fund shares to meet different investor needs (e.g. retail vs. qualified plans).

ETF class benefits:

Broader access, asset growth, lower costs.

Efficient rebalancing, lower transaction costs, better index tracking.

Mutual fund class benefits:

In-kind transactions → tax efficiency.

Cost savings from leveraging ETF scale.

Access to established securities lending programs.

Is there a (tax) catch? Possibly.

The petition includes some wording cautioning that when a mutual fund class redeems shares, it may force the fund to sell securities, creating taxable events for all shareholders, including ETF class holders.

I’ll just point out that this hasn’t been an issue in most Vanguard funds, which rarely, if ever, make distributions.

While this is big, there’s still a ways to go….

“The Hottest Thing In ETFs?”

Yeah, it’s tax.

I’ve only scratched the surface on this, but the Disruptive ETFs, and the growth of the ETF share class could each be huge. They probably won’t drive another $10 trillion in AUM… but maybe they could.