Will seeding ETFs in-kind go mainstream? "I doubt it"

The largest ETF sponsors need to drive costs lower, but they have little incentive to help.

Seeding an ETF in-kind using Section 351 conversion is not new.

But Meb Faber’s new ETF, with the cheeky ticker TAX, is getting some attention because he’s invited the general public to seed it in-kind.

“If you truly understand the implications, this should be a tectonic shift for the asset management industry,” Meb said in a LinkedIn post a month ago.

I wrote an explainer here and dove deeper here, and then I hosted a LinkedIn Live event with Meb here and compared it with the exchange fund here.

Then, out of nowhere, Benjamin Clark, a software engineer and kindred spirit, asked if I wanted to collaborate on an article exploring a future where Section 351 conversion was cheap and plentiful. What would that unlock?

The short answer is a reality where investors don’t consider tax when reallocating to or between ETFs. We call this the Routine Rebalancing Utopia.

We conclude the Routine Rebalancing Utopia won’t happen, partly because it is too investor-friendly.

We think the largest ETF sponsors must drive the costs of Section 351 conversion to zero, but they have little incentive to do so.

However, all hope is not lost. If enough investors see enough value in frictionless rebalancing, that could disrupt the status quo. We examine one case that could catalyze the entire movement.

But let’s start at the beginning.

Wargaming the 351 conversion

Does the industry have sufficient incentive to drive the cost of Section 351 conversion to zero?

To figure this out, Benjamin and I assumed the incremental cost and risk of contributing assets to an ETF in-kind via Section 351 is zero.

If true, assets flow into and between ETFs without trading. And investors realize no capital gains or tax drag.

Since the Code only allows seeding ETFs in-kind, ETF sponsors must continue launching ETFs but may usually merge them without tax consequence under Section 368 (examples: Fidelity, Vanguard).

Under these circumstances, we see the following possibilities:

More strategies seeded in-kind

Less asset stickiness

Tax-free rebalancing

Personalized glide paths

Better credit lines and rates

If Section 351 conversion were cheap and plentiful, investors could easily convert separate account assets into the ETF wrapper without realizing capital gains.

ETF sponsors would then compete with each other through what Benjamin calls “the next stage in the cheap beta wars” by offering a wide selection of strategies, launching as regularly as monthly (Calamos has already achieved this frequency in its Structured Protection ETFs).

Asset stickiness would then drop to zero, and investors would migrate to and between the ETFs that best address their risk, cost, and tax preferences.

Tax, as an investment friction, would disappear. Therefore…

Cheap and plentiful Section 351 conversion is very investor-friendly

Once assets are in the ETF wrapper, Section 351 conversion affords lookthrough treatment, so satisfying its diversification provision is simple.

Investors would begin using Section 351 for routine rebalancing.

We say the industry has achieved Routine Rebalancing Utopia when investors no longer consider tax when reallocating to and between ETFs

Ubiquitous Section 351 conversion would allow the tax deferral benefits of the ETF wrapper to be expanded to the entire portfolio. While this is technically possible with a fund-of-funds ETF, a fund-of-funds is not customizable, while a personal portfolio of ETFs is.

For example, the target date fund could be redefined to meet the needs of individual investors and gradually transition tax-free as the investor’s circumstances change.

A side effect of de-risking a portfolio may be more (and less costly) margin, which may be used for further investment or consumption.

We believe the largest ETF sponsors need to drive the cost of Section 351 conversion to zero because they control most ETF assets.

Unfortunately for investors, the largest ETF sponsors are not sufficiently threatened by smaller ETF sponsors and lack the incentive to make Section 351 conversion more efficient.

Not a credible threat

While small and mid-sized ETF sponsors may continue attracting assets using Section 351 conversion as a sales tactic, the largest ETF sponsors will likely take action only if they feel threatened.

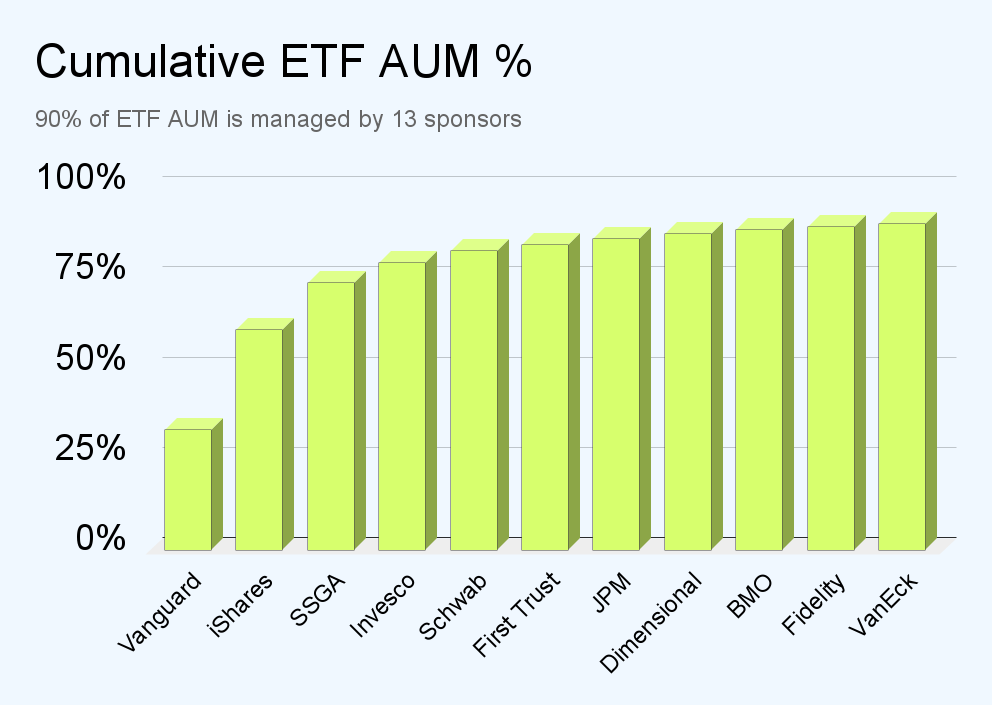

This seems unlikely given that the largest three sponsors (Vanguard, BlackRock, State Street) control over 70% of all ETF assets, and the top 13 ETF sponsors manage around 90% of all ETF assets.

Without large incumbent participation, Section 351 conversion will stay niche.

An elephant does not care about a mosquito. And the largest ETF sponsors do not care about occasional challenges from smaller sponsors… usually. Later, we explore a case where they might.

At this point, we’re looking for a reason for the incumbents to take action. The threat is insufficient, but perhaps they have sufficient incentive?

Sufficient incentive?

Returning to the question, “Does the industry have sufficient incentive to drive the cost of Section 351 conversion to zero?” We think not.

The largest ETF sponsors gain little by making Section 351 conversion more efficient:

Tax helps them keep the assets they already have

351 conversion offers little incremental marketing or sales benefit

It may cannibalize higher-fee products

“Cannibalization doesn’t create the best circumstances for innovation,” said Mike Allison, a portfolio manager for Eaton Vance’s exchange fund and equity option income products for over 20 years and runs the New Lantern Hedged Equity Fund.

To be fair, we could flip each of these points on its head.

Tax-free reallocation could help incumbents win assets

351 conversion might be another arrow in the distribution quiver

Cannibalizing higher-fee products is better than having them leave altogether

But we felt the following tradeoffs would block innovation:

Preference for product stickiness to fluidity

Preference for simplicity over operational complexity and risk

Unknown retail demand

Making matters worse, appealing to retail investors with the promise of tax-free reallocation to ETFs is expensive.

The cost of achieving Routine Rebalancing Utopia

“I doubt it,” Wes Gray, a principal at ETF Architect, who has managed several Section 351 conversions, said via email when I asked him if he thought we would ever achieve Routine Rebalancing Utopia.

In reality, there are substantial costs to making a Section 351 conversion available to the public, including marketing, client service, operations, and counsel, increasing the already-high barrier to launching an ETF.

Wes has little reason to bullshit. ETF Architect could make a lot of money if Section 351 conversions became ubiquitous.

“We would usually do [351 conversions] for large single families,” the head of a mid-sized ETF sponsor, who wished to remain anonymous, told me, “But they don’t make sense for the largest ETF sponsors to open to the public… it is more hassle than it is worth.”

What about mutual funds?

We’re hunting for sufficient threat or incentive to kick the largest ETF sponsors into action.

Since mutual funds are horribly tax-inefficient, isn’t there some motivation for smaller ETF sponsors to capture those assets through Section 351 conversion? Isn’t that a credible threat?

Although it’s legally possible to use a Section 351 conversion to get mutual funds into the ETF wrapper, an authorized participant will not redeem mutual funds in-kind. Mike Allison explained they are a “cash in, cash out” vehicle.

Achieving tax-efficiency with mutual funds will likely instead come from the ETF share class many mutual fund sponsors have recently petitioned to add. Those assets get the ETF wrapper without the Section 351 conversion.

So, if the largest ETF sponsors are insufficiently threatened or incentivized, could market demand change that… um… eventually?

While the Section 351 conversion solves many problems. They are all niche.

A niche solution

Achieving Routine Rebalancing Utopia requires threat or incentive, which may be achieved through a large-scale shift in demand.

However, Section 351 conversion mostly solves niche cases.

For example, conversion combines disparate, though already diversified, assets from separate accounts into the ETF wrapper. This might include direct indexing portfolios that are “locked up” (well above cost basis) or other broadly diversified baskets of assets that could benefit from the operational efficiency of the ETF wrapper.

While putting this article together, one adviser at a large multi-family office suggested the following scenario:

Suppose an investor has adopted a tax-aware long-short strategy, like the 130/30

After several years, the investor wishes to unwind the short positions

The adviser nets several shorts and longs to defer capital gains

But the resulting portfolio is “chunky” (though sufficiently diversified)

In this case, a 351 conversion into a fully diversified ETF could meaningfully reduce risk and unlock the operational efficiency of the ETF wrapper without tax drag

These situations are increasingly common but still niche.

The only thing that will spur the Section 351 conversion to the mainstream is substantial investor demand, which we examine next.

Routine Rebalancing Utopia hinges on investor demand

In one possible case, Mike Allison suggested that “stranded” index ETF assets – those well above cost basis – could be converted via Section 351 into hedged equity ETFs.

This scenario checks two important boxes.

Large: Millions of proximate retirees could benefit

Consistent: 10,000 Baby Boomers retire every day

The vast retirement and de-risking of Boomers assets could be a significant enough shift for smaller ETF sponsors to mount a credible threat to the largest ETF sponsors.

In that scenario, the largest would have to respond by offering new ETFs seeded in-kind. This could be the beginning of Benjamin’s aforementioned product war.

However, the hedged equity scenario may only drive mass adoption of Section 351 conversion in that particular instance. Hedged equity is tiny today (maybe $20 billion in assets). It could get bigger but in the order of trillions? It’s hard to say.

Meb Faber gets credit

We believe the largest ETF sponsors lack sufficient threat or incentive to introduce Section 351 conversion and drive costs down. In other words, something big would have to change to get their attention.

That said, Meb gets credit for putting his money where his mouth is and building in public.

On December 18, 2024, his Cambria Tax Aware ETF (ticker TAX) will go live.

Everyone can inspect daily holdings and see if the public-facing Section 351 conversion successfully attracted assets.

We will cover that event to get a data point on retail demand.

That’s possibly where the “tectonic shift” could begin, but the road is long.